--- title: "QQQ's Worst Day of 2026: The Jobs Report That Markets Read the Wrong Way" subtitle: "A 172K NFP beat triggered a tech-led selloff.

Here's what the data actually said — and why Trump told Wall Street it should have rallied." canonical_url: https://pragmatic.mortgage/news/qqq-worst-day-2026-jobs-report-tech-selloff published_at: 2026-06-05T18:30:00Z author: Pragmatic Mortgage Lending kicker: MARKETS · RATES · REAL ESTATE reading_time: 8 min ---

The number on the tape

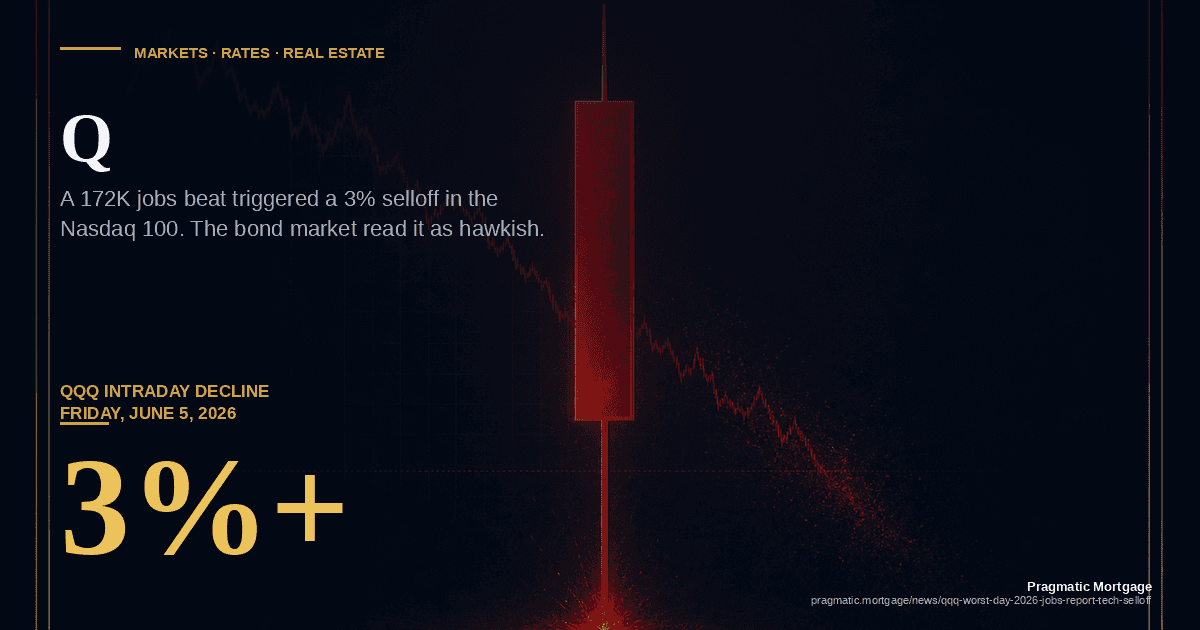

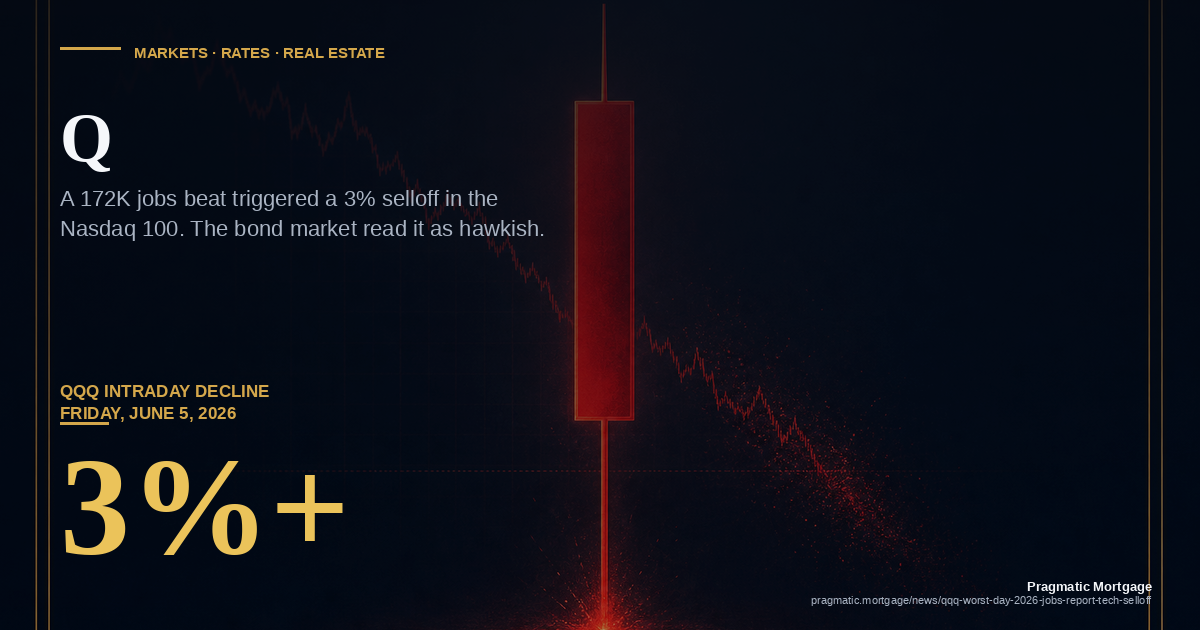

The Invesco QQQ Trust fell more than 3% on Friday, June 5, 2026 — the worst single-day decline for the Nasdaq 100 ETF in 2026.

The S&P 500 gave back roughly 1.6%, the Russell 2000 shed 1.7%, and the Dow bucked the trend with a small green close.

The 10-year Treasury yield jumped back to 4.46%, the highest level in a month.

The Bloomberg Dollar Spot Index added about 0.4%. Bitcoin slid toward $63,000.

The catalyst was a single print: the May U.S. Nonfarm Payrolls report, released at 8:30 a.m.

ET by the Bureau of Labor Statistics. The U.S. economy added 172,000 jobs in May.

The unemployment rate ticked up to 4.3% from 4.2%. Average hourly earnings rose 3.9% year over year.

Consensus had been calling for 130,000 to 140,000 jobs, with the unemployment rate steady at 4.3%. The headline beat was real, but not enormous — and the unemployment rate moved in the wrong direction for a "hot" report.

Yet the market reaction was unambiguous: bonds sold off first, then equities. Tech led the move. The long end of the curve did most of the damage.

—

What the market actually read

The first read was wrong, and the market knew it within minutes.

The naïve read is: more jobs = stronger economy = higher growth = stocks up.

That was Donald Trump's read.

Within an hour of the print, the President posted on Truth Social that the market reaction was "surprising" and that "stocks should go up, not down" on a jobs beat.

The framing made sense at a gut level: 172,000 is a healthy number in a year when economists have been quietly debating whether the U.S. was even adding 100,000 a month.

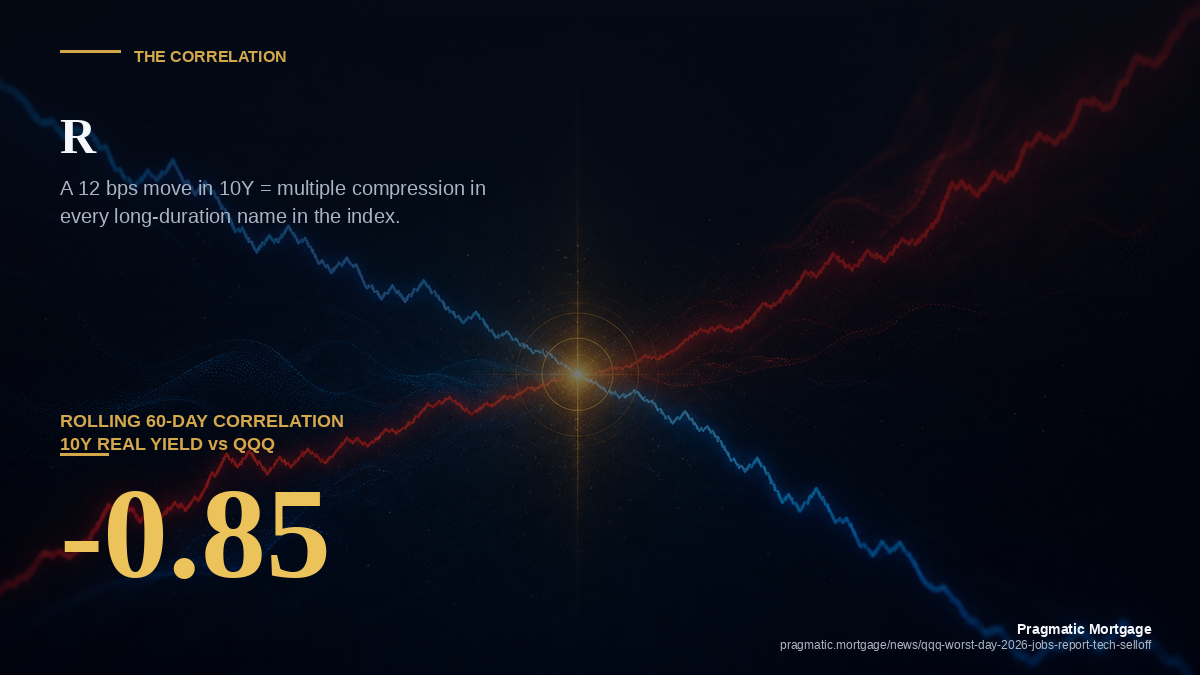

But that's not what the bond market traded on, and the bond market leads the equity market when rates are the binding constraint.

What the rates market actually read was

▪ The cuts are gone. Fed funds futures priced out the second 2026 cut entirely. Implied odds of a September move collapsed from roughly 60% Thursday afternoon to under 18% by Friday's close. The terminal rate for 2026 is now closer to 4.00% than 3.75%.

▪ The curve steepened, badly. The 2s10s spread steepened to +62 basis points — the widest in nearly a year. Long duration got hit hardest, which is why QQQ, the AI trade, and the high-multiple software names sold off first.

▪ Wage stickiness is back. 3.9% year-over-year average hourly earnings is above the Fed's stated comfort zone. With services inflation still running hot, the bond market concluded the disinflation story is on hold — not reversing, but paused.

▪ Geopolitical oil is the new floor. Brent crude is holding above $96 with the Iran conflict unresolved and the House having just passed a war powers resolution the President is expected to veto. That keeps the inflation breakeven propped up, which keeps real rates elevated, which is poison for long-duration tech cash flows.

The result: a jobs beat is now a bad jobs beat, because the only way to get one is for the labor market to stay tight enough to keep wages, services inflation, and core PCE all uncomfortably above target.

—

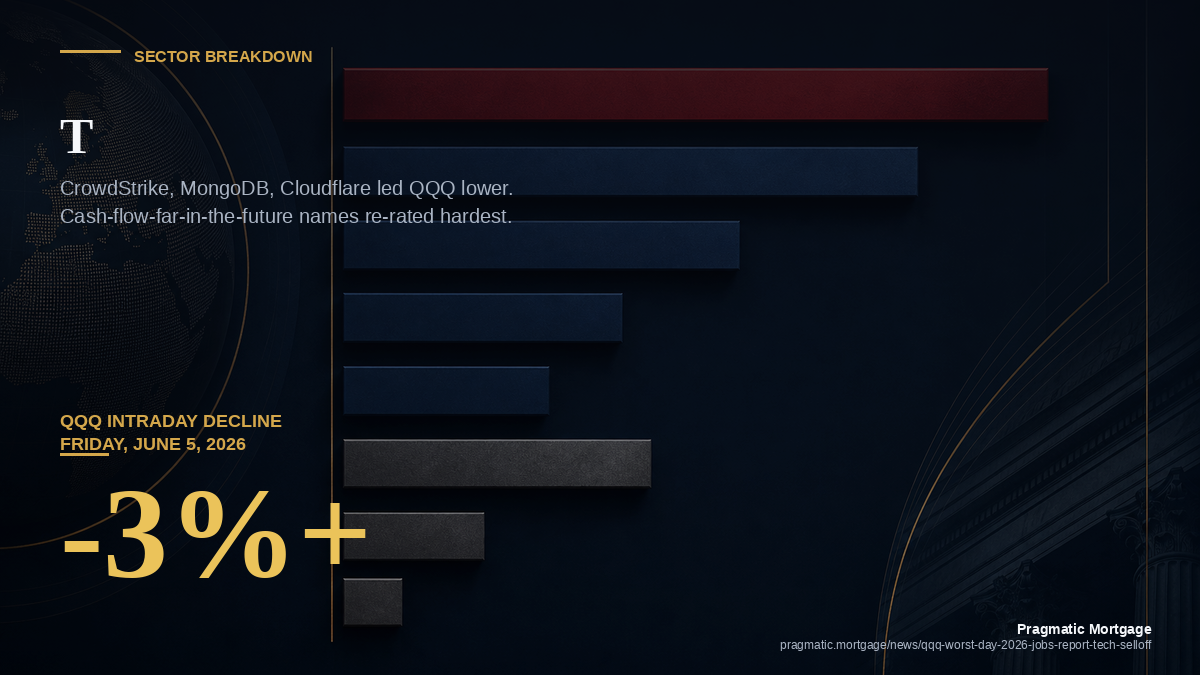

Why this hits tech twice as hard

The Nasdaq 100's weight in AI, semiconductors, and recurring-revenue software makes it a duration asset in disguise. When real yields rise, the present value of those long cash-flow streams compresses harder than for cyclicals, banks, or energy names.

You can see it in the Friday tape

▪ CrowdStrike, MongoDB, and Cloudflare were the biggest drag on QQQ — all three are cash-flow-far-in-the-future names.

▪ Apple and Microsoft underperformed the index modestly, not because their earnings deteriorated, but because their duration profile is longer than the bond market is currently rewarding.

▪ The chip trade caught a second wind of bad news. Broadcom's Q3 guidance, which had looked extraordinary on Wednesday after-hours, was being re-discounted on Friday as investors noticed the AI-semi capex story now requires even more long-dated cash flow to justify the multiples.

▪ Crowdstrike, Marvell, and Super Micro all sold off on company-specific news layered on top of the rate move.

Goldman's Christian Mueller-Glissman told clients on Friday that the selloff was — quote — "a healthy sign" and that "probably not a bad idea to see a bit of consolidation". That's the right read for anyone with a 3–5 year horizon.

It's cold comfort if you're a leveraged long or a pension allocator marking books on June 30.

—

Trump vs. the tape

By early afternoon, the President was on Truth Social again, more pointed this time. The substance of his complaint was the same: the data is good, the market is wrong, somebody explain this to me.

The Hill's reporting on Friday captured the mood: a jobs beat that should have triggered a relief rally was instead read as a forward-looking inflation warning. The disconnect is genuine, and it tells you something important about the regime markets are pricing for the second half of 2026.

There are three possible reads of the move

- Markets are wrong. The Fed will look through a single strong print, the unemployment rate is up, and 3.9% wage growth isn't the same as 4.5%. Rate cuts get pushed to October, not cancelled. This is the administration's read, and the Goldman read, and probably the right read for the next 2–4 weeks.

- Markets are right and the Fed is behind. The May print is the second consecutive upside surprise. The Beige Book released this week flagged inflation rising "at a moderate to strong pace" on the back of the Iran oil shock. If June comes in hot, the Fed is forced to hold for the rest of the year. The dollar stays bid, the curve stays steep, and QQQ bleeds for another 5–7% from here before anyone believes in year-end multiples again.

- *Markets are right about the direction but wrong about the speed.* Cuts are delayed, not cancelled. The Fed wants to see two more months of disinflation evidence before it acts. The QQQ pain is real but bounded — a summer consolidation, not a regime change.

The honest answer is that nobody knows, including the Fed. Powell's replacement, Kevin Warsh, takes the baton at the next FOMC.

The Reuters Friday afternoon wire called the jobs report "hawkish" and flagged Warsh's well-known rate-hawk priors as an additional reason the front end is repricing.

What you can say with high confidence: the easy money in 2026 is not in long-duration tech, it's in shorter-duration cash, short-term Treasuries, and dividend-paying value. That trade worked in May. It worked again on Friday. It's likely to keep working through the summer.

—

The Canadian tie-in (it's not forced)

This is where the U.S. story becomes a Canadian real estate story, and it isn't a stretch.

Canadian fixed mortgage rates are priced off Canadian 5-year Government of Canada bond yields, not U.S. Treasuries.

But the two move together more often than not, and the direction of Friday's move matters on both sides of the border.

Three channels from the U.S. tape into Canadian housing

▪ The Bank of Canada is now boxed in. The BoC was already reluctant to cut further after the April decision. With the U.S. long end backing up 12 basis points on Friday, the odds of a July BoC cut dropped from 35% to under 15% on swap-market screens.

If you're a variable-rate borrower or a buyer waiting for a trigger-rate reset, the trigger isn't coming next month.

▪ The 5-year GoC yield is following the 10-year UST up. Friday's Canadian bond selloff was smaller than the U.S. move, but the 5-year GoC yield still closed 6 basis points higher. That translates almost mechanically into the fixed-mortgage specials at the big banks within 1–2 weeks. If you locked a 5-year fixed last month at 4.39%, that trade looks smart today.

▪ The U.S. labor market affects Canada too. The Brookings Institution's midweek analysis — which Fortune reported on Friday — flagged that aggressive U.S. immigration enforcement had cost the U.S. economy an estimated 668,000 jobs so far.

That bleeds north.

Canada is pulling skilled trades, healthcare workers, and tech labor from the same global pool.

A tighter U.S. labor market keeps Canadian wage growth from collapsing, which keeps Canadian services inflation sticky, which is the BoC's main reason not to cut.

For the Canadian real estate angle, the cleanest framing is:

- If you have a renewal coming in the next 6 months, the window to lock a 5-year fixed at sub-4.5% specials is closing. The best pricing available right now is likely the best you'll see for the rest of 2026.

- If you're a variable-rate borrower, your trigger rate is not getting a relief cut in July. Plan for the path that takes you to your renewal.

- If you're a buyer waiting on rate cuts to bring sales volumes back to 2021 levels, those buyers are still on the sidelines because the cuts aren't coming. The listing-inventory story in Toronto, Vancouver, and Calgary is not a 2026 story — it's a 2027 story at the earliest.

—

The outlook: neutral, by design

We don't make directional calls on the Nasdaq. We do make calls on rate paths, and the call right now is neutral-to-cautious on further cuts.

What to watch over the next four weeks

▪ June CPI (release date: July 11). If core CPI prints under 0.2% month-over-month, the September cut comes back. If it prints at 0.3% or higher, the curve steepens again and QQQ tests the May lows.

▪ The June NFP (release date: July 5). The single most important data point. A print under 130,000 reframes everything; a print over 160,000 confirms the Fed is on hold for the year.

▪ The Q2 earnings season (starts mid-July). The hyperscalers, Nvidia, and the big software names will set the AI-trade narrative.

If guidance re-affirms the 2027 capex spend, the multiple compression stops. If any of them blink, QQQ has another 5–8% to give back.

▪ Iran resolution or escalation. A genuine ceasefire drops oil to $80 and changes the inflation trajectory. A Hormuz incident sends it to $120 and forces the Fed to hike.

The base case is neither — a long, grinding stalemate that keeps oil in the $90s.

▪ SpaceX IPO pricing (filed for the week of June 12, $1.75T implied valuation). Whether this prints cleanly is a read on overall risk appetite. A pulled or down-sized deal is a yellow flag for the whole AI/capex complex.

The bottom line

—

A 3% down day in QQQ is not a crash. It is the market repricing the cost of money, and it is doing so in the open. The risk is that the repricing has another 2–3 months to run before the Fed gives the all-clear.

For Canadian borrowers, the same repricing is already in the 5-year GoC curve. The decisions worth making in the next 30 days are mortgage decisions, not market-timing decisions.

—

What we'd actually do

This isn't financial advice. It's the framework we use with our own clients.

If you have a mortgage renewal inside 12 months

call your broker this week. The best 5-year fixed specials are still in the 4.39% – 4.59% range at the major lenders, with a handful of monoline lenders offering 4.29% on insured switches. Those specials will likely be gone by the July BoC meeting.

If you're shopping for a variable rate

don't. Not because variable is wrong in principle, but because the trigger-rate math doesn't work in your favour with the BoC on hold. Pay the small premium for fixed and own the certainty.

If you're a real estate investor in a major market

the 2026 thesis is cash flow, not appreciation. The buyers who closed in 2021 are not coming back to bid prices up.

The buyers who matter are renters-by-choice and move-up buyers who finally have two years of stable payments. Underwrite to rent, not to flip.

If you're a passive equity investor in QQQ

this is the moment a balanced allocation earns its keep. A 60/40 portfolio held up materially better on Friday than a 100% Nasdaq-100 allocation. Rebalancing bands and disciplined contributions are the unglamorous discipline that works in months like this one.

—

The bottom line

The May 2026 jobs report was a beat, not a blowout. The market reaction was sharp but orderly.

The Fed's next move is data-dependent in a way it hasn't been since 2007. The QQQ selloff is a symptom — a reflection of how much of the 2025 rally was bought with the assumption that the Fed would be cutting into a slowing labor market. That assumption is now on hold.

For a Canadian mortgage holder, the question is the same one the bond market asked on Friday: how much higher for how much longer?

The honest answer at the end of the first week of June 2026 is: higher, and longer than the market was pricing a week ago.

The opportunity is the same one it's been all year — for borrowers who can move, to move now. For everyone else, to plan as if the BoC and the Fed both hold into the fall, because that's what the curve is telling us today.

—

This article is for informational purposes only and is not financial, investment, or mortgage advice. Data sourced from the Bureau of Labor Statistics (BLS), Bloomberg, Reuters, The Hill, FXStreet, Goldman Sachs research, the Bank of Canada, and Industry Canada as of market close June 5, 2026. All figures in CAD or USD as noted.