Canada just slipped into a technical recession — here’s what it actually means for real estate

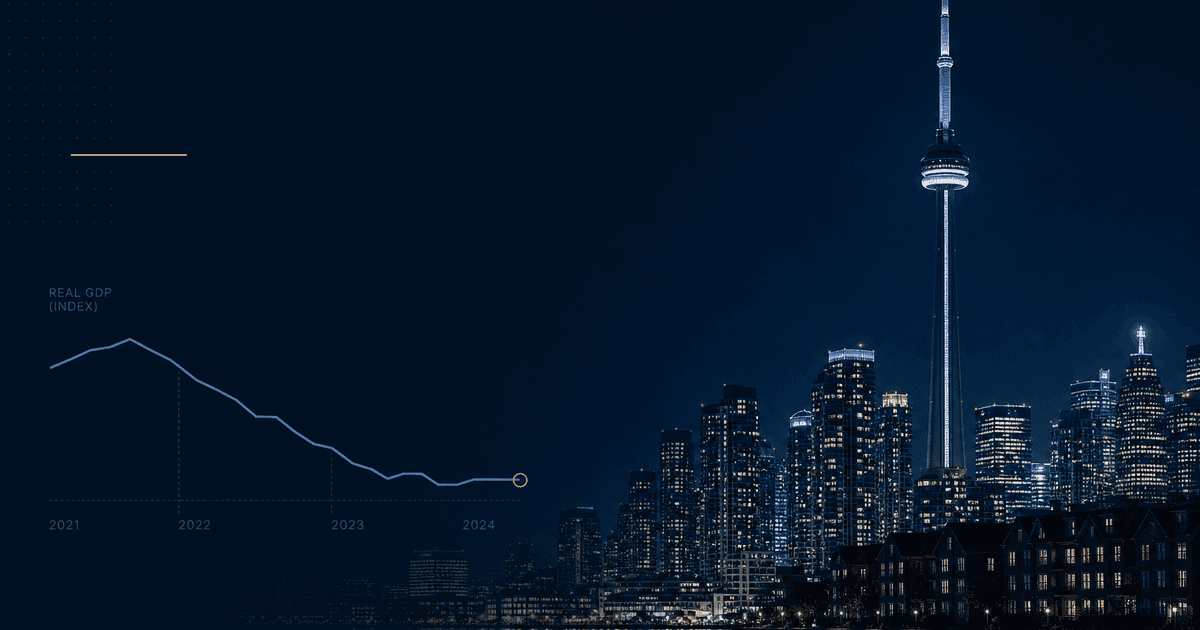

Canada’s latest GDP report came with the kind of headline that gets attention fast: technical recession. But the most important part of the story is not the label — it’s the mix of signals underneath it.

The official quarterly numbers show an economy that is weak, but not collapsing.

Real GDP was flat in Q1 2026 after a 0.2% decline in Q4 2025.

On a per-person basis, real GDP actually rose 0.2%, because the population declined for a second straight quarter.

Household spending still increased 0.4%, while business capital investment fell 0.7%.

That combination matters. It tells you Canadians are still spending, but businesses are more cautious. It also tells you the economy is under strain, but not in a straight-line freefall.

What the data actually said

The recession headline is based on a classic rule-of-thumb: two weak quarters in a row. But the details make this a more nuanced story.

- Real GDP: flat in Q1 2026

- Q4 2025: down 0.2%

- Per-capita GDP: up 0.2%

- Household spending: up 0.4%

- Business capital investment: down 0.7%

In other words: the economy slowed, but the household side was not uniformly falling apart. The weakness is showing up more clearly in business investment and confidence than in a broad consumer collapse.

So what does “technical recession” actually mean?

A technical recession is a signal, not a full diagnosis.

It usually means the economy has lost momentum for long enough that output is no longer expanding in a meaningful way. But it does not automatically mean:

- mass layoffs everywhere,

- a housing crash,

- a financial crisis,

- or a nationwide collapse in demand.

That’s why the headline can sound scarier than the underlying data. A technical recession is often the point where policy makers, lenders, and consumers start asking the same question: is this a short slowdown, or the start of something worse?

Why the outlook still matters more than the headline

For markets, the next few months matter more than the label.

If inflation stays contained and the Bank of Canada gets more room to support growth, rates may ease further or remain stable enough to help borrowing conditions. If labour markets weaken more sharply, though, the slowdown can spread from “caution” into “cut back.”

That is the fork in the road for housing

- Best case: slower growth, lower rates, stable employment, and a housing market that cools without breaking.

- Weaker case: softer jobs, weaker confidence, and more buyers sitting on the sidelines.

The economy can look fragile without triggering a crash. But once employment and confidence turn together, real estate usually feels it quickly.

What this could mean for Canadian real estate in the short term

Short term, the most likely effect is selectivity.

That usually shows up as

- longer days on market,

- fewer bidding wars,

- more conditional offers,

- more price sensitivity,

- and more regional differences.

In markets that were already stretched — especially parts of the GTA, GVA, and condo-heavy investor markets — even a modest economic slowdown can cool activity faster than in more balanced areas. Buyers become more careful. Sellers who need to move may have to negotiate more.

This is why “Canada housing” is too broad a phrase to be useful. Different regions react differently depending on:

- local employment,

- inventory levels,

- affordability,

- investor concentration,

- and whether the market is still being supported by population growth and limited supply.

What this could mean long term

Long term, a technical recession does not automatically break the housing market.

Canada still has structural housing issues: limited supply in many regions, uneven affordability, and ongoing demand pressures that don’t disappear just because GDP prints soft for a quarter or two.

The long-run housing outlook will depend on three things more than the recession label itself:

That’s why the more likely long-term outcome is regional rebalancing, not a single national outcome.

Some markets may see prices flatten, some may correct, and some may simply move sideways for a while. But the broad story is not “housing is doomed.” The story is more like: the market is becoming more selective, more regional, and more sensitive to employment and rates.

The bottom line

Canada’s technical recession headline is real — but the interpretation needs nuance.

The economy is clearly softer than it was. Still, the data says slowdown, not collapse.

For real estate, that means the near-term outlook is likely to be more cautious and more regional, while the long-term outcome will still hinge on rates, jobs, and supply.

If you’re watching Canadian housing right now, the most important question is not whether the word recession appears in the headline. It’s whether the weakness spreads into the labour market and confidence enough to change buying and selling behaviour for longer.

Sources

- Statistics Canada, Q1 2026 GDP release

- Reuters reporting on Canada’s technical recession framing

- Bank of Canada Market Participants Survey / outlook commentary

- CMHC and housing market outlook materials