For three years, Canada has lived inside a single question

When does the housing market actually crash?

It is the question that has delayed first-time buyers into their late thirties, pushed renewers into longer amortizations, and convinced a generation that the right move was to wait.

It is also, as of the Canadian Real Estate Association's May 2026 forecast update, no longer the right question to ask.

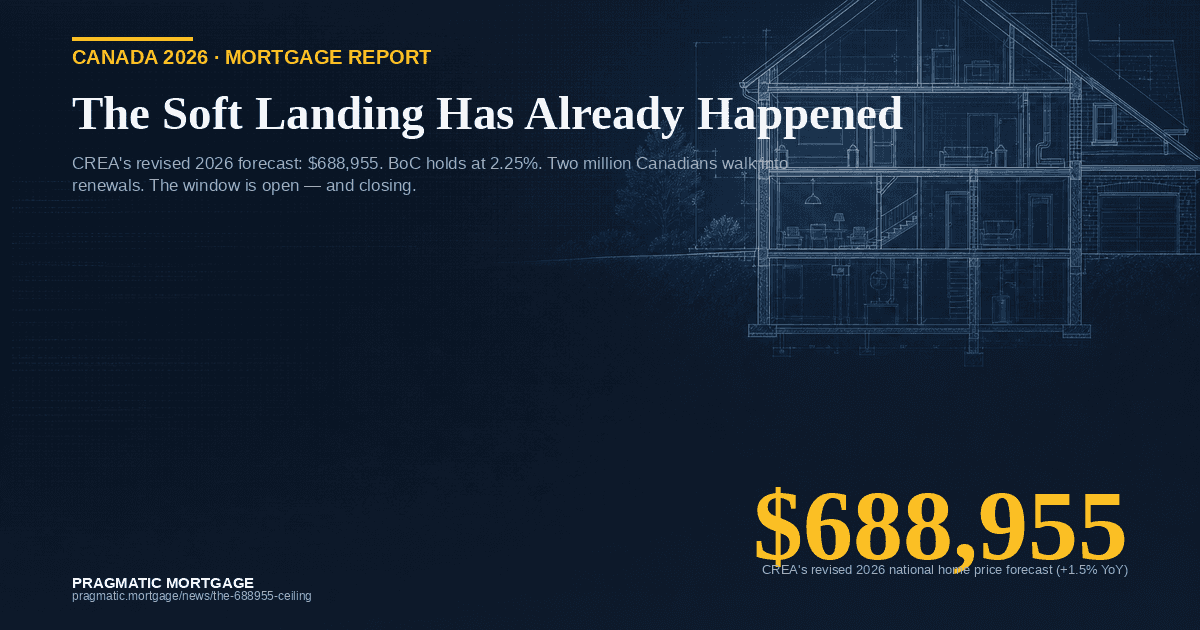

CREA revised its 2026 national average home price forecast to $688,955 — a roughly 1.5% gain over 2025, down from the 3% it was projecting three months ago.

In plain terms: flat.

Not falling. Not recovering. Flattening into a thin margin that has very little room to absorb another shock.

The "crash" most people were waiting for has already quietly landed. It just didn't look like one.

---

The number that should change the conversation

The headline: $688,955.

The subhead: it is essentially the same number the market was sitting at in early 2024.

The mechanics behind the downgrade matter more than the number itself. Three forces are converging:

▪ BoC policy rate held at 2.25% (April 29, 2026) — the third consecutive hold, with the next decision on June 10, 2026.

▪ ~2 million Canadian households are walking into a mortgage renewal decision this year, the bulk of them at materially higher rates than they signed for in 2020–2021.

▪ The $1.5M insured-mortgage cap is now the binding ceiling for first-time buyers in Toronto, Vancouver, and Ottawa — and the 30-year amortization for first-time buyers and qualifying new builds is the structural lever pulling monthly payments back into reach.

Read those three together and the picture is not collapse. It is a market in which the government has effectively rebuilt the floor under the demand side, while the supply side is finally catching up.

---

Why the 2008 mental model is wrong

Most of the "waiting for the crash" crowd is still running a 2008 script.

That script assumes a 30% peak-to-trough correction, a wave of forced sales, and a fire-sale moment for patient cash buyers.

None of that is in the 2026 data.

What the data shows instead is a structural correction driven by policy, not panic:

▪ Immigration targets have been pulled back sharply. Population growth in 2025 was the slowest in nearly a decade, and 2026 is tracking lower. That removes the demand pressure that defined 2020–2023.

▪ Rental completions are at a multi-decade high. Purpose-built rentals delivered in 2024–2025 are now hitting the market, easing the pressure that pulled buyers out of renting and into ownership.

▪ Regional divergence is real. CMHC's latest outlook still has Ontario prices declining modestly through 2026, while Alberta and the Prairies are flat-to-up. Calling "Canada's housing market" one thing in 2026 is a category error.

The buyers and brokers still waiting for a 2008-style moment are not just late. They are waiting for an event that the policy stack has structurally prevented.

---

The renewal math that no one is talking about

The 2-million-renewal number is the story inside the story.

Roughly 60% of Canadian mortgages renewing in 2025–2026 will face higher monthly payments than they were paying on their original term.

For the median Canadian household, that is a payment shock of $300–$700 per month.

Not catastrophic. But exactly the kind of cash-flow squeeze that delays a kitchen reno, postpones a second child, and pushes the next purchase further down the road.

Three things to know about the renewal wave

1. It is not a default wave.

Canadian mortgage holders are unusually well-capitalized by international standards. Stress tests at origination (the 2% above contract rate rule) cushioned the original affordability. The renewal pinch is real, but it is a cash-flow story, not a foreclosure story.

2. It is a competitive story for brokers.

Clients renewing this year are shopping. Lenders are quietly repricing retention products.

The spread between a client's existing lender's renewal offer and a broker-arranged alternative is the largest it has been in a decade. This is the single most actionable moment in the 2026 mortgage market for the broker channel.

3. It is a story about the 30-year amortization, used carefully.

Extending amortization lowers the monthly payment but extends the interest timeline. For a renewer whose cash-flow crunch is 24–36 months long, that is a sensible bridge.

For a renewer who could afford the original payment, it is a quiet tax on the future. The conversation a broker has with that client in Q3 2026 matters.

---

The June 10 decision

The Bank of Canada next announces on June 10, 2026.

The consensus expectation is a hold at 2.25%, with the more aggressive forecasters split between a 25bp cut (if Q2 GDP undershoots) and a 25bp hike (if the tariff-driven inflation pulse from Q1 persists).

The bigger story is not the June decision.

It is the trajectory.

RBC's most recent forward guidance has the policy rate rising toward 3.25% by the end of 2027 as the BoC normalizes away from emergency settings. If that path holds, the cheapest-mortgage window of the decade closes in the next 12–18 months.

Not because the BoC is hawkish. But because 2.25% is, in historic terms, unsustainably accommodative for an economy growing at potential.

For first-time buyers sitting on the fence: the rate environment of 2026 is not the rate environment of 2027.

---

What the soft landing actually means

"Soft landing" is a phrase that gets used loosely. In 2026, it has a very specific meaning in the Canadian context:

For sellers — Pricing realistically is no longer optional. The multiple-offer era is over. Properties that price to current comps sell; properties that price to 2022 comps sit.

For buyers — The window for a real negotiation is open, and it is open right now. The $1.5M insured cap, the 30-year amortization, and a 2.25% policy rate are the most buyer-favorable macro stack since 2019. But it is a window, not a permanent condition.

For renewers — This is the most actionable quarter in years. Shop. Do not auto-renew. The lender you started with is not, on average, offering the best 2026 product for your file.

For brokers — The 2026 book of business is renewal-driven, not purchase-driven. Build the renewal pipeline now, because the Q4 wave is coming.

---

The pragmatic take

There is no crash coming in 2026. There is also no rocket.

The market is doing the unglamorous, important work of finding a level that policy can sustain, that lenders can underwrite, and that buyers can actually afford.

The Canadians who will come out of this cycle well are not the ones who timed the bottom. They are the ones who made decisions inside the window when the window was open.

$688,955 is not a disaster. It is not a triumph.

It is, finally, a number the market can hold.

---

📖 Read the full deep-dive on the blog → pragmatic.mortgage/news/the-688955-ceiling

📌 Save this post. The June 10 BoC decision will reshape a few of the numbers above. We will update.

---

Sources & data points

▪ CREA May 2026 Home Price Forecast Update ($688,955, +1.5% YoY — revised down from 3.0%)

▪ Bank of Canada policy rate decision, April 29, 2026 (held at 2.25%); next decision June 10, 2026

▪ BoC Household Financial Survey: ~60% of renewing mortgages face higher payments

▪ OSFI B-20 stress test guidance (qualifying rate at +2% above contract)

▪ CMHC Housing Market Outlook, Q1 2026 (Ontario price declines persisting; Prairies/Atlantic flat-to-up)

▪ RBC Forward Guidance, May 2026 (policy rate path toward 3.25% by end-2027)

▪ Statistics Canada population estimates, Q1 2026

▪ CMHC rental completions data, 2024–2025 vintage