Your CCB and GST Credit Just Hit. Here's How to Use Them on Your Mortgage.

The Canada Child Benefit and the quarterly GST/HST credit payments landed in Canadian bank accounts this week. For millions of households, that's anywhere from a couple hundred dollars to several thousand — predictable, recurring, and easy to overlook.

Most of the advice you'll see today is about how to spend that money.

This guide is about how to use it.

Not in a get-rich-quick way. In a "few hundred dollars applied at the right moment, on the right product, in the right account, actually changes your mortgage math over the next 5 to 25 years" way. That's a real number. We'll walk through it.

---

What's actually landing in Canadian bank accounts this week

Two distinct payments, paid by direct deposit or cheque on a fixed federal schedule:

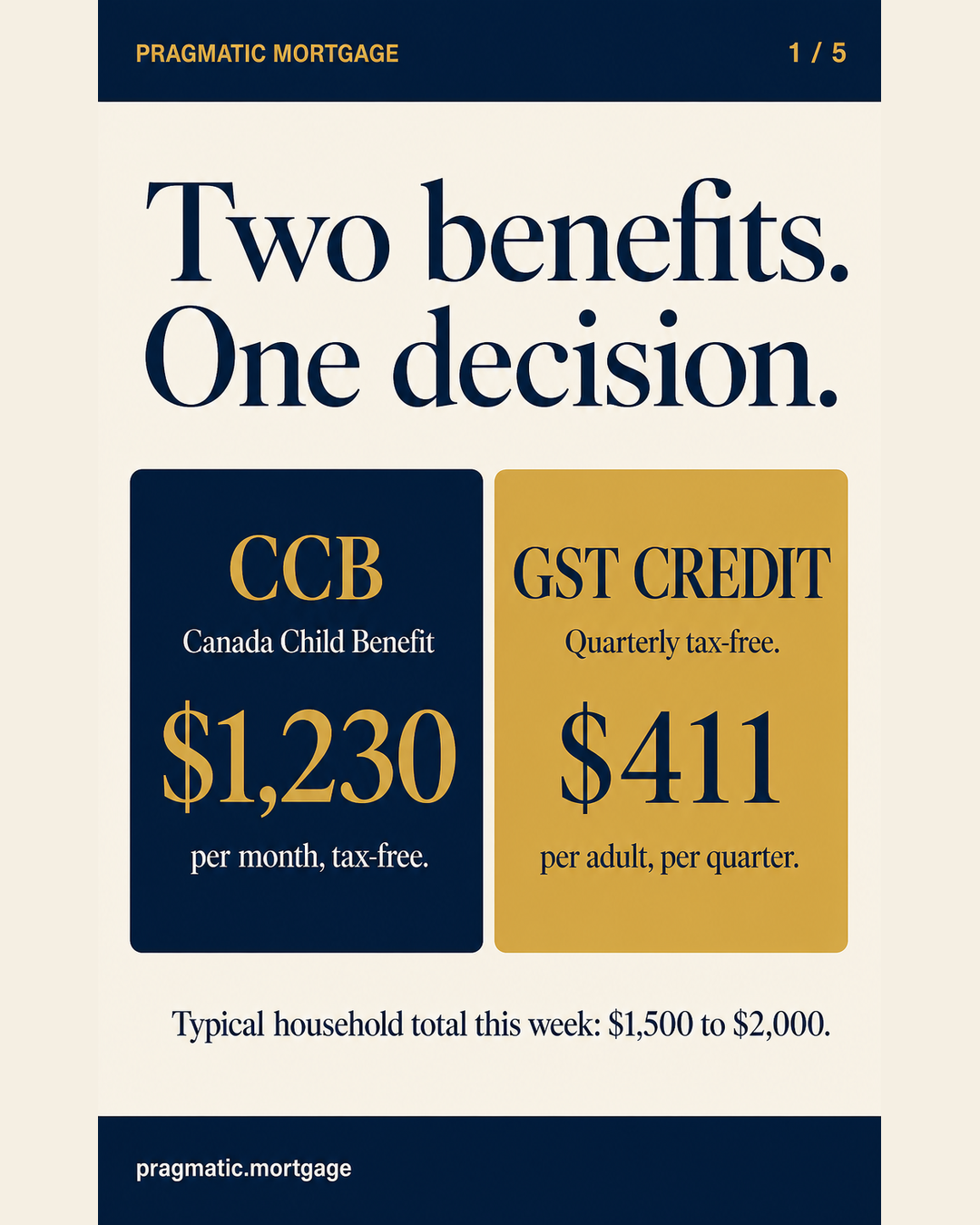

- Canada Child Benefit (CCB) — tax-free, monthly, paid to eligible families with children under 18. Maximum annual amount for 2026 is $7,997 per child under 6 and $6,748 per child aged 6–17, indexed to inflation and reduced at higher family incomes. For a two-child household under the income cutoff, that's roughly $1,230/month, before any provincial top-ups.

- GST/HST Credit — tax-free, paid quarterly (July, October, January, April). Maximum annual amount for 2026 is $533 per adult, $289 per child, plus a single supplement of up to $181 for low-income working households.

Together, for a typical two-parent, two-child household with modest income, you're looking at roughly $1,500 to $2,000 in your account this week. For a single low-income earner with two kids, it's closer to $2,400 for the quarter. For a high-income family, it tapers to zero.

Those are real numbers. The question is what they do when you put them somewhere specific.

Slide 1: A typical two-parent, two-child household is receiving roughly $1,500 to $2,000 this week between CCB and the July GST/HST credit payment. Source: Government of Canada benefit rate tables, 2026.

---

What most people do (and why it's fine, but not optimal)

Three common patterns

- Spend it. Groceries, kids' activities, a bill that's been nagging. This is real life. Nobody should be shamed for using benefit payments to cover the cost of raising kids in 2026.

- Park it in a savings account. Safe, liquid, but at current HISA rates of roughly 3 to 4 percent, you're earning something — and losing something bigger to inflation if the account isn't tax-sheltered.

- Do nothing and let it sit in chequing. Surprising how common this is. The money gets blended into monthly cash flow and disappears.

None of those are wrong. But there's a fourth option that almost nobody talks about, and it's the one that has the biggest long-term impact per dollar.

---

Apply it directly to your mortgage — the math, in plain English

Canadian mortgages have three structural features that most people forget exist

- Prepayment privileges. Every federally regulated mortgage in Canada comes with the right to prepay up to 15% of the original principal balance per year, on top of your regular payments, without penalty. Some lenders allow more. Some allow double-up payments. Some allow both. The exact rules are in your mortgage contract.

- Prepayments go directly to principal. When you make a prepayment, the entire amount reduces the principal balance. There's no tax on it. There's no fee. The next interest charge is calculated on the smaller balance. The effect compounds.

- Prepayments shorten your amortization, not your payment. This is the part most people miss. You keep making the same monthly payment. The mortgage just finishes sooner — and you pay dramatically less interest in total.

Here's what a single CCB or GST payment does when applied as a mortgage prepayment:

Slide 2: Worked example. $1,500 prepayment on a $400,000 mortgage at 4.04% (current 5-year fixed benchmark), applied in month 30 of a 25-year amortization, saves approximately $2,400 in interest and shortens the mortgage by roughly 4 months. Source: Pragmatic Mortgage Lending calculation, current posted 5-year fixed rate.

---

The number, broken down by household

Let's run a few common scenarios. Assumptions: a $400,000 mortgage at the current 5-year fixed benchmark of 4.04%, 25-year amortization, prepayments applied in the month they're received, mortgage term renewed at the same rate for simplicity.

- $500 prepayment, applied once: Saves roughly $800 in interest, shaves about 2 months off the amortization. Small but real.

- $1,500 prepayment, applied twice a year (matching the CCB + GST/HST rhythm): Saves roughly $4,800 in interest, shaves about 8 months off the term.

- $2,000 prepayment, applied four times a year (matching every quarterly GST cycle plus both CCB months): Saves roughly $9,500 in interest, shaves about 16 months off the term.

- $300/month continuous prepayments from a parent's CCB-only entitlement, applied automatically: Saves roughly $18,000 in interest over the remaining term, shaves about 2.5 years off the amortization.

These are not aspirational numbers. These are the actual outputs from current posted mortgage rates with no rate-cut optimism baked in.

Slide 3: Side-by-side comparison of four prepayment patterns applied to a $400,000 mortgage at 4.04% over a 25-year amortization. The compounding effect is non-linear — small recurring prepayments beat a single large lump-sum by total interest saved.

---

The three common mistakes

These are the patterns we see most often when households come in for advice after the fact.

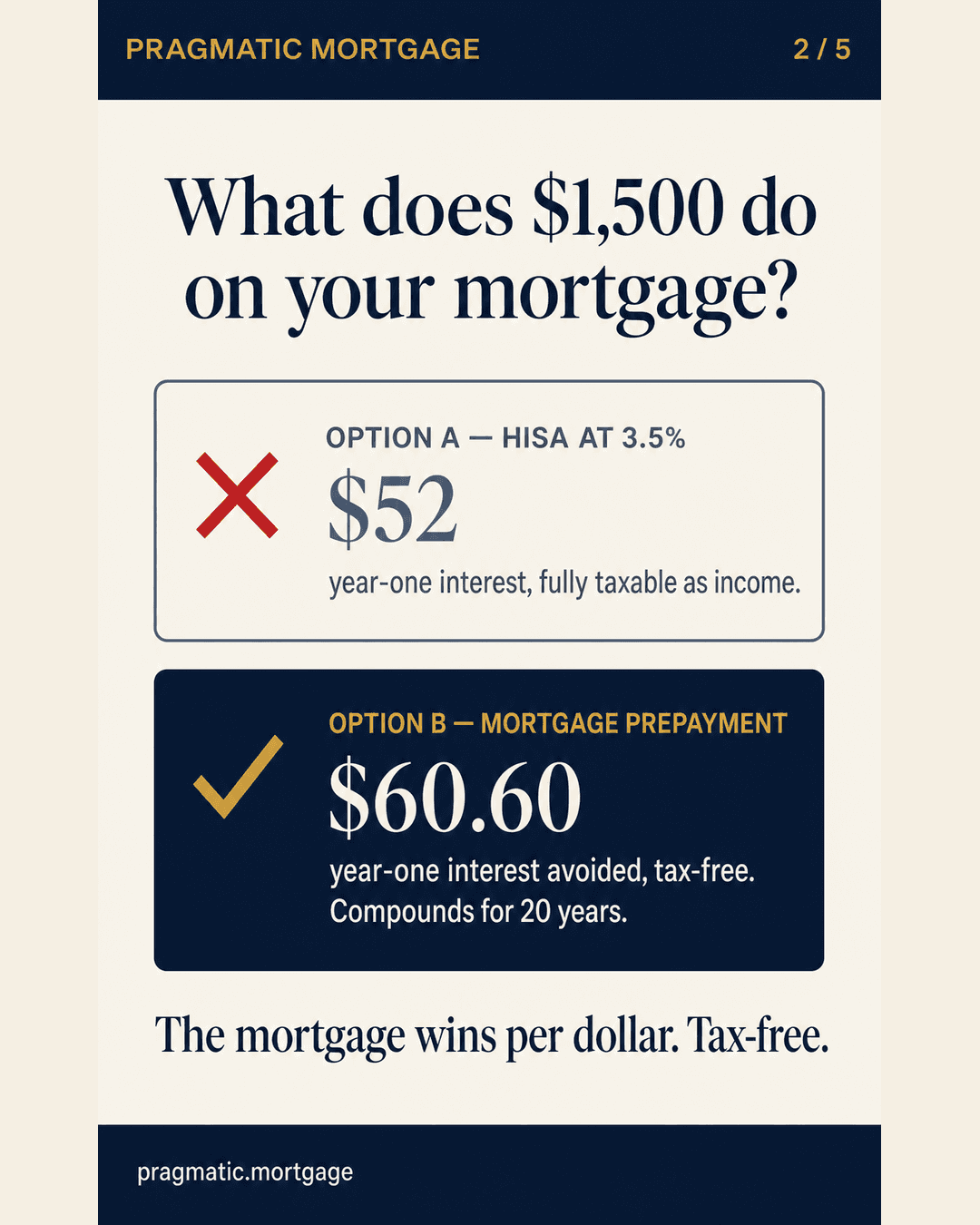

Mistake 1: Putting it in a savings account instead. A HISA at 3.5% pays you roughly $52 in year one on a $1,500 deposit, fully taxable.

The same $1,500 as a mortgage prepayment at 4.04% "earns" $60.60 in year-one interest you no longer pay.

The mortgage path is bigger, tax-free, and compounds.

The savings account is more liquid — which is a real reason to choose it, but it shouldn't be the default by inertia.

Mistake 2: Treating it as a "bonus" and spending it on a one-off. A $1,500 purchase depreciates. A $1,500 prepayment compounds for 20 years.

The decision is not "spend vs. save" — it's "spend vs. invest in the single largest asset most Canadians will ever own."

Mistake 3: Missing the annual reset. Most mortgage prepayment privileges reset on the mortgage anniversary date, not the calendar year.

If your mortgage started in March 2025, your 15% annual limit resets in March 2026 — not January.

This matters when stacking prepayments from CCB and GST credits across a year: if you time them around your mortgage date, you get maximum flexibility.

Slide 4: The "mortgage anniversary reset" is the most overlooked feature in Canadian mortgage contracts. It also determines the optimal timing for any series of prepayments across the year.

---

A five-minute checklist you can do today

Before you decide what to do with this week's payment, run through these

- ☐ Pull your current mortgage statement. Note the current balance, the remaining amortization, and your mortgage anniversary date.

- ☐ Find your prepayment clause. Look for "prepayment privilege," "annual prepayment limit," and "double-up payment" in your contract. The exact wording matters.

- ☐ Calculate your unused prepayment room. Multiply your original principal by 15%. Subtract any prepayments you've already made this year. That's your remaining headroom.

- ☐ Decide your cadence. If CCB arrives monthly and you have unused prepayment room, a small monthly prepayment is mechanically the most powerful option. If GST arrives quarterly and you don't have monthly headroom, mark the calendar.

- ☐ Check your HISA balance. If you have more than three months of emergency fund sitting in a non-registered savings account, the mortgage prepay is likely the better return per dollar — even before tax.

If you've done the checklist and the math doesn't make sense, that itself is useful information. It means you have headroom, or a great rate, or an emergency-fund gap. Each of those has a different answer.

---

When NOT to use the money for a mortgage prepayment

A few honest cases where spending or saving beats prepaying

- You have high-interest debt. If you're carrying a credit card balance at 19.99% or a line of credit at 9%, paying that down first beats prepaying a 4% mortgage.

- Your emergency fund is under three months of expenses. A prepayment is irreversible in the short term. Pulling money back out of your mortgage is expensive.

- Your mortgage is up for renewal within 12 months. Some lenders restrict prepayments in the final 30 to 90 days. Check before you act.

- You're in a variable-rate mortgage with payment shock concerns. A prepayment still helps, but if your payment has increased because of rate changes, focus on stabilizing cash flow first.

- You have a defined goal for the money in under two years — a Reno, a vehicle, a planned move. Don't lock capital into a 25-year instrument if you need it back soon.

Slide 5: Five situations where spending or saving the CCB/GST payment beats prepaying your mortgage. Each one is a signal to talk to a broker about your full picture.

---

The bottom line

The Canada Child Benefit and the GST/HST credit are designed to help Canadian households with the cost of living. How you use them is your call.

For most Canadian households with a mortgage and some unused prepayment room, applying the payment directly to the mortgage is the highest-return option per dollar, tax-free, with compounding for the rest of the term.

For households in any of the situations above, it's not. The right answer is the one that matches your full picture — and a five-minute conversation with a broker who can run the actual numbers on your mortgage is usually the fastest way to know.

Either way, the worst option is the one where the money sits in chequing and disappears into the rhythm of the month without a decision being made.

---

This article is for general information only.

Mortgage prepayment rules vary by lender, product, and contract.

Verify your specific prepayment privileges with your current lender or a licensed broker before applying.

CCB and GST/HST credit amounts depend on family income, number of children, and marital status — refer to your most recent Notice of Assessment or CRA My Account for the exact figures that apply to you.