The BoC's 25% House-Price Scenario: What It Actually Says, What Would Have to Break, and Why Your Mortgage Isn't Automatically Doomed

Here is what the Bank of Canada actually published, where the 25% number comes from, and what both sides of the balance sheet look like.

Where the 25% number actually came from

The 25% figure is not a 2026 forecast. It comes from the Bank of Canada's 2026 Financial Stability Report, released on May 28, 2026 by Senior Deputy Governor Carolyn Rogers and Deputy Governor Toni Gravelle.

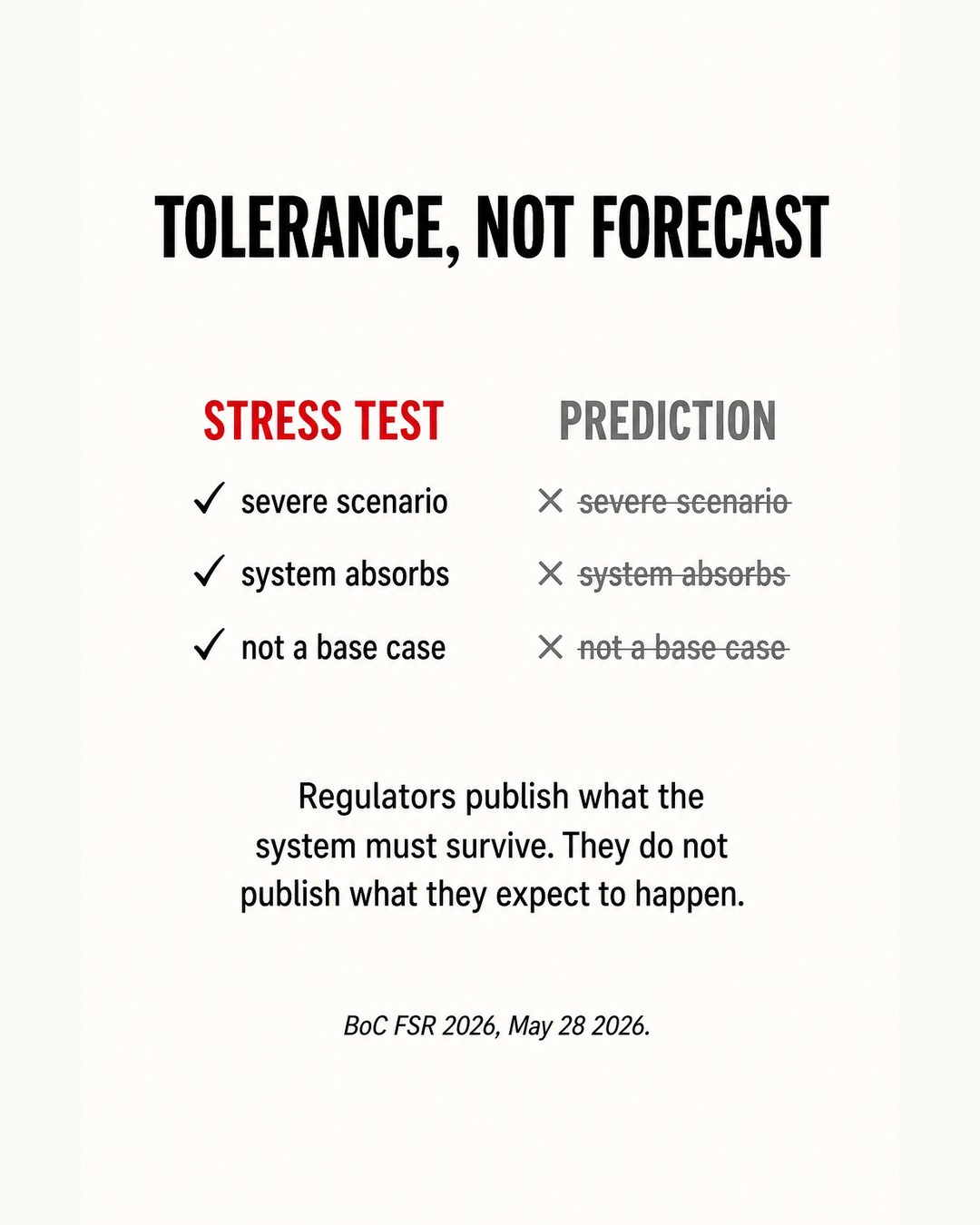

In it, the Bank models one severe but illustrative scenario — the kind regulators are required to run, not the kind they expect to happen.

The 2026 scenario stacks two shocks at once

- A sustained period of high global oil prices linked to the war in the Middle East.

- A sharp sell-off in global equity markets.

Under that combined shock, the Bank's own modelling produces roughly

- Real GDP falling about 1% from peak to trough.

- The unemployment rate spiking to roughly 10%.

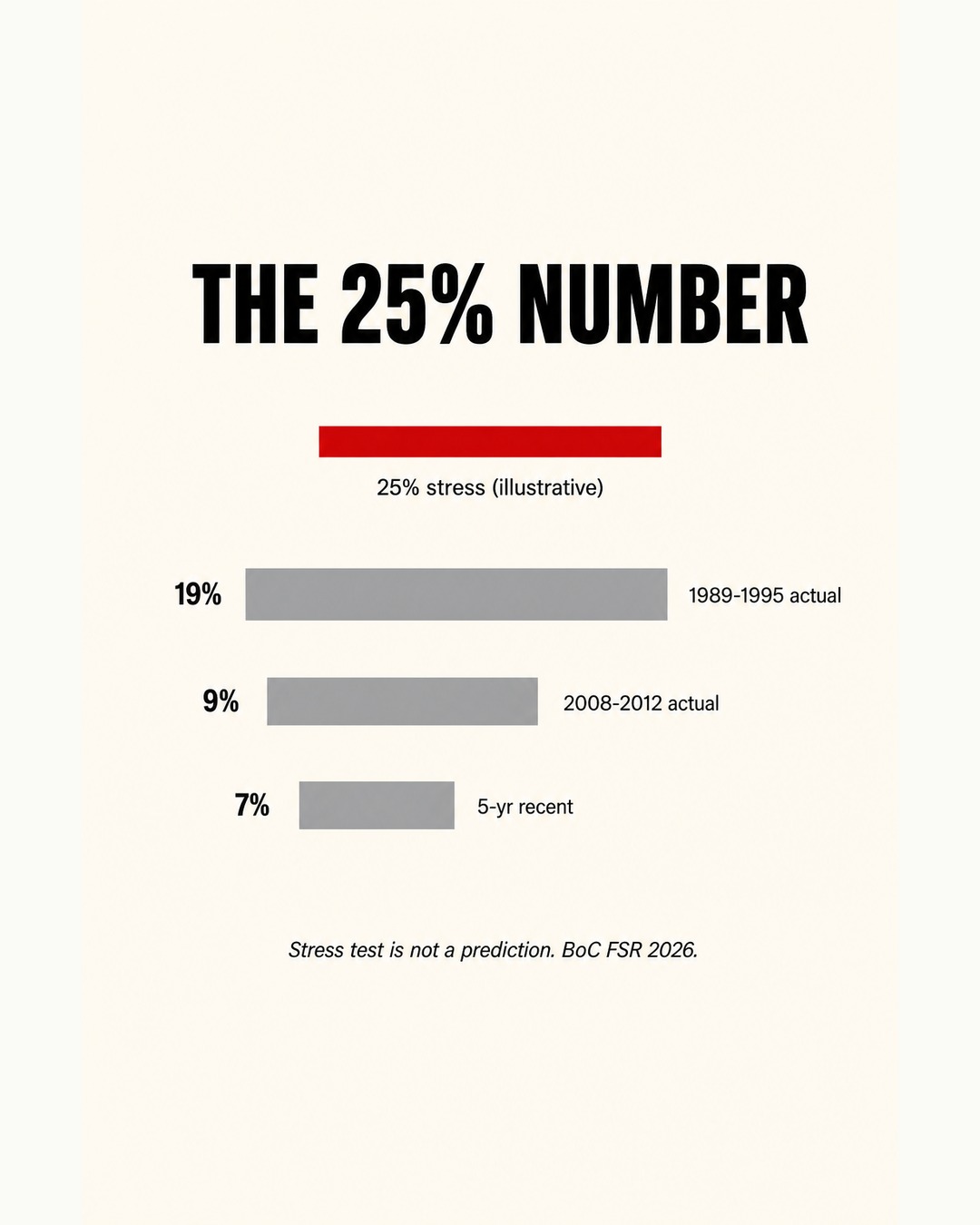

- Canadian home prices falling about 25%.

The Bank is explicit, in both the FSR and the press conference, that this is not a forecast, that it carries no probability weight, and that the FSR is "an assessment of how existing vulnerabilities could amplify shocks," not a prediction that they will.

A separate, older 25%-ish number exists in the 2025 FSR's FSAP stress test (peak-to-trough house-price decline of 26%, with unemployment at 9.2% and GDP down 5.1%). That was a trade-war stress test, run jointly with the IMF, and it tested bank solvency — not house prices in isolation.

Some of the viral videos are quietly sliding between the 2025 FSAP number and the 2026 FSR number as if they were the same scenario. They aren't.

What the underlying data actually shows right now

The "what if unemployment spikes" framing collapses a few things that the Bank deliberately keeps separate. Here is the baseline the FSR itself reports as of May 2026:

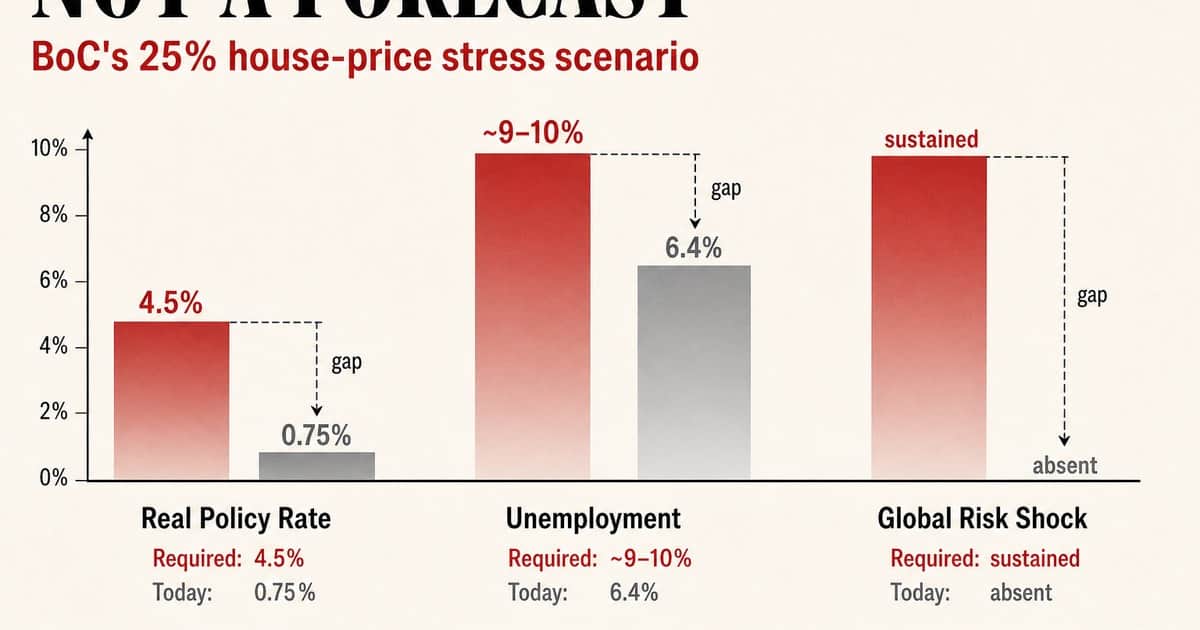

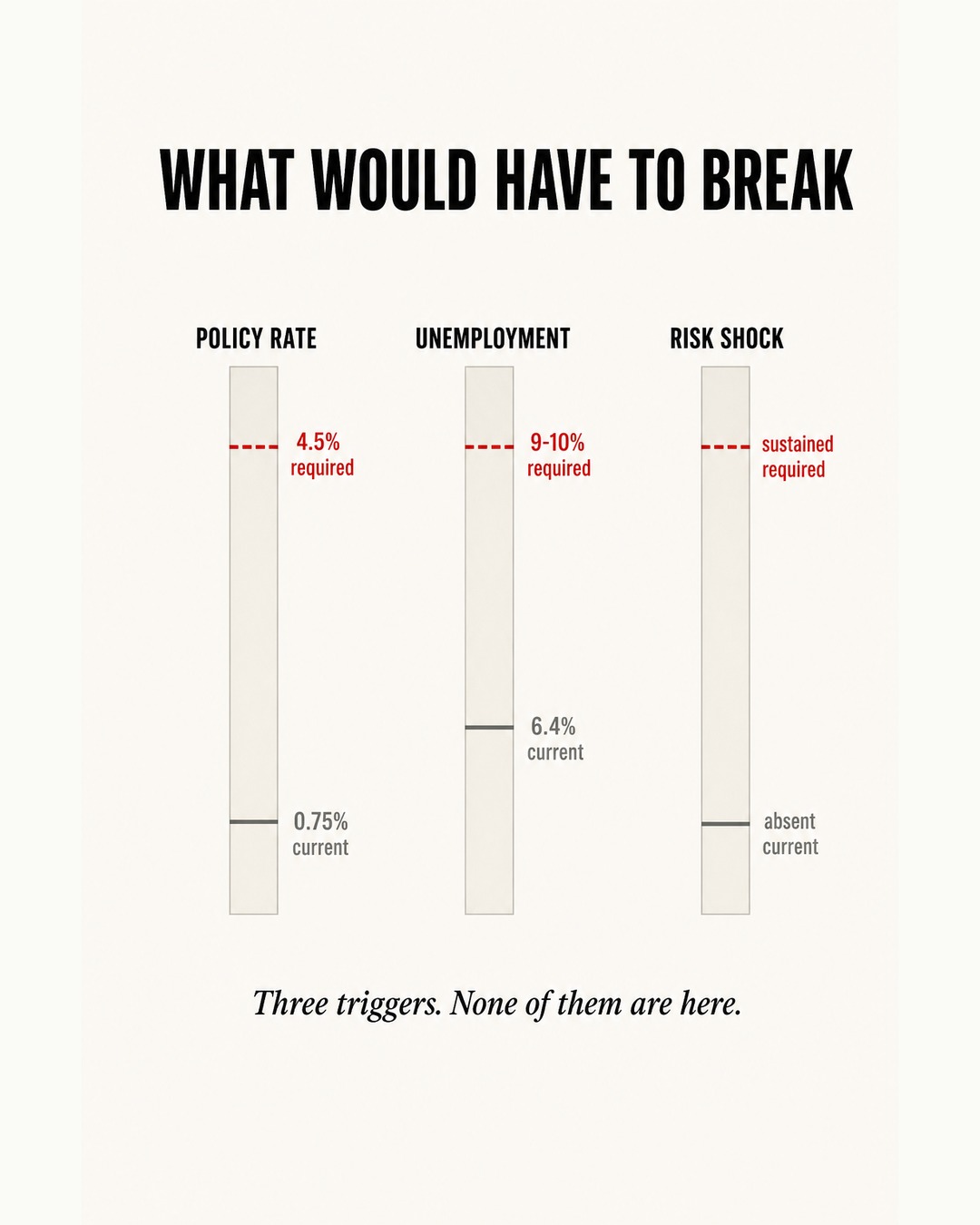

- Unemployment has been stuck in a 6.5%–7% band for the past 12 months — high by Canadian historical standards, the highest in the G7, but stable, not spiking.

- The typical Canadian home price is already down about 5% year-over-year, and down about 20% from the 2022 peak. The 25% headline number is, in many markets, closer to where prices already are than where they might go.

- Mortgage arrears remain low. About 1.3% of mortgage holders are more than 60 days behind on a payment, only slightly above the 2018–19 average. For households without a mortgage, the rate is about 2.5% — also stable.

- The mortgage stress test is doing its job. More than 90% of borrowers who renewed in the last 12 months did so at rates below the qualifying rate they were originally stress-tested at. They were already qualified to handle a higher payment than they're now actually paying.

- The "mortgage renewal cliff" is mostly behind us. About 12% of outstanding mortgages are still facing a renewal over the next 12 months, with an average payment increase of about 15%. By the second half of 2027, the Bank expects nearly all the pandemic-era payment shocks to have fully played out.

In other words: Canadian households have been running this stress test in slow motion for three years now, and the system has, so far, absorbed it. The arrears data is the proof, and it doesn't match the panic framing.

The bear case: where the 25% scenario could actually start to bite

A balanced read of the FSR is not the same as dismissing the risk. There are three places where the severe scenario has real, identifiable exposure:

- The Toronto 2022–23 condo cohort. The Bank specifically calls out stress as "most acute among Toronto area borrowers who took out a mortgage in 2022–23." These borrowers locked in at the peak of the rate-hiking cycle, often on pre-construction assignments, on properties that have since seen the steepest price declines. They represent only about 2% of outstanding balances — small in aggregate — but concentrated enough that further price declines in this slice are realistic.

- The refinancing cliff. At current home prices, the Bank estimates only about 4% of borrowers won't be able to refinance at renewal in 2027. If home prices fall another 10%, that share rises modestly to about 7% nationally — but to roughly 12% in the Toronto area. The mechanism is straightforward: lower equity means harder to qualify, which means a forced sale or a longer amortization becomes the only way out.

- Trade-exposed small business. The Bank's other severe channel is small and medium-sized businesses with high leverage, low margins, and concentrated exposure to U.S. trade. A sustained tariff shock would push unemployment up not by abstract macro mechanics, but by laying off workers in specific tradeable sectors. The unemployment spike and the price decline in this scenario are not independent — they feed each other, which is what makes the 10% unemployment + 25% price combination internally consistent in the model even if it sounds extreme in isolation.

There is also a secondary amplifier the FSR highlights: hedge funds now buy 40–50% of new Government of Canada bond issuance, mostly using short-term repo borrowing.

A loss of repo access could trigger forced bond sales, spike government yields, and force the Bank of Canada to choose between fighting the yield spike or fighting the recession.

This is not a house-price channel directly, but it is a stress amplifier that the 2026 FSR treats as a top-tier vulnerability.

The bull case: why the 25% number is unlikely to materialize on its own

The 2026 FSR is also clear that the Canadian financial system has handled repeated shocks over the past year without broad-based stress. The reasons the severe scenario is genuinely severe — i.e., unlikely to be the path we actually walk — are structural:

- Banks are unusually well capitalized. Large Canadian banks' CET1 ratios averaged 13.3% in early 2025, about 2 percentage points above late 2019.

- Provisions for credit losses are up 8% year-over-year.

- The IMF/BoC stress test in the 2025 FSR showed that even in the deeper 26%-house-price-decline trade-war scenario, large bank capital stayed well above regulatory minimums.

- The transmission mechanism from "house prices fall" to "banks fail to lend" — the one that turned 2008 into a global crisis — is materially weaker in Canada than it was in the U.S. fifteen years ago.

- The mortgage market is stress-tested, not just insured. Canadian borrowers qualify at the greater of their contract rate plus 2% or 5.25%. That is the rule that kept 2022–24 renewals from producing the wave of forced sales the doomsayers predicted. It is not a perfect filter — and the 2% of Toronto 2022–23 borrowers the Bank flags are the ones who slipped through — but it has demonstrably done the work it was designed to do.

- The "trigger" for the 25% scenario is oil + equities, not unemployment per se. This is the framing the Bank itself uses, and it matters. Unemployment can rise for many reasons; a 10% spike with a 25% house-price decline only happens in the model when it's combined with a sustained oil shock that prevents the Bank from cutting rates. Without that combination, the house-price channel in isolation is much weaker. The Bank's own 2025 trade-war FSAP scenario (with a 26% house-price decline) requires a deep, persistent trade shock — not just a jobs number.

- Wealth buffers are still positive on net. The Bank notes that household net worth has continued to grow, driven by financial asset gains, even as housing wealth has softened. Debt-to-net-worth is well below pre-pandemic averages. Most borrowers who renewed in 2025 had built enough savings to cover a year of higher payments from financial assets alone.

What an honest read of the FSR actually says

If you strip the FSR of its scenario language and read it as a status report, the message is closer to: the system has absorbed a lot already, the remaining known risks are concentrated in identifiable cohorts, and the next 12 months are the last big test of pandemic-era mortgage assumptions.

The 25% headline number is a real model output under a real, but tail-risk, combination of shocks. It is not a baseline.

It is not a forecast. It does not require only "unemployment spiking" to land — it requires oil staying high, equities selling off, trade tensions escalating, and the Bank being constrained from cutting rates. Each of those has a meaningful probability. The combination does not.

What to actually watch over the next 12 months

If you're making a mortgage, renewal, or purchase decision in the back half of 2026, the FSR's own risk indicators are a more useful checklist than the 25% headline:

- The 25% number is worth understanding. It is not worth panicking over.

The data says the Canadian mortgage system is doing the work it was designed to do, the bank balance sheets are doing the work they were designed to do, and the most exposed slice of borrowers is small enough to be a policy problem, not a market problem.

None of that means prices can't fall further from here.

It means the path to a 25% decline runs through a specific, identifiable set of triggers — and the absence of those triggers is itself information.

---

Sources

Bank of Canada, Financial Stability Report 2026 (May 28, 2026); Bank of Canada 2025 Financial Stability Report and FSAP stress test (May 2025); BoC press conference opening statement, May 28, 2026; The Globe and Mail, "Geopolitical, trade risks pose rising threat to financial stability, Bank of Canada warns," May 28, 2026; CMHC Housing Market Outlook 2026; BoC rate decision announcement, June 10, 2026.