A Toronto Star headline this June declared that more Ontarians are missing mortgage payments, citing a 52% jump in the "balance delinquency rate" over a single year.1 That headline is technically accurate. It is also missing the context that explains why the number moved, where it sits historically, and which borrowers are actually feeling it.

Here is the data, on its own.

The number, plain

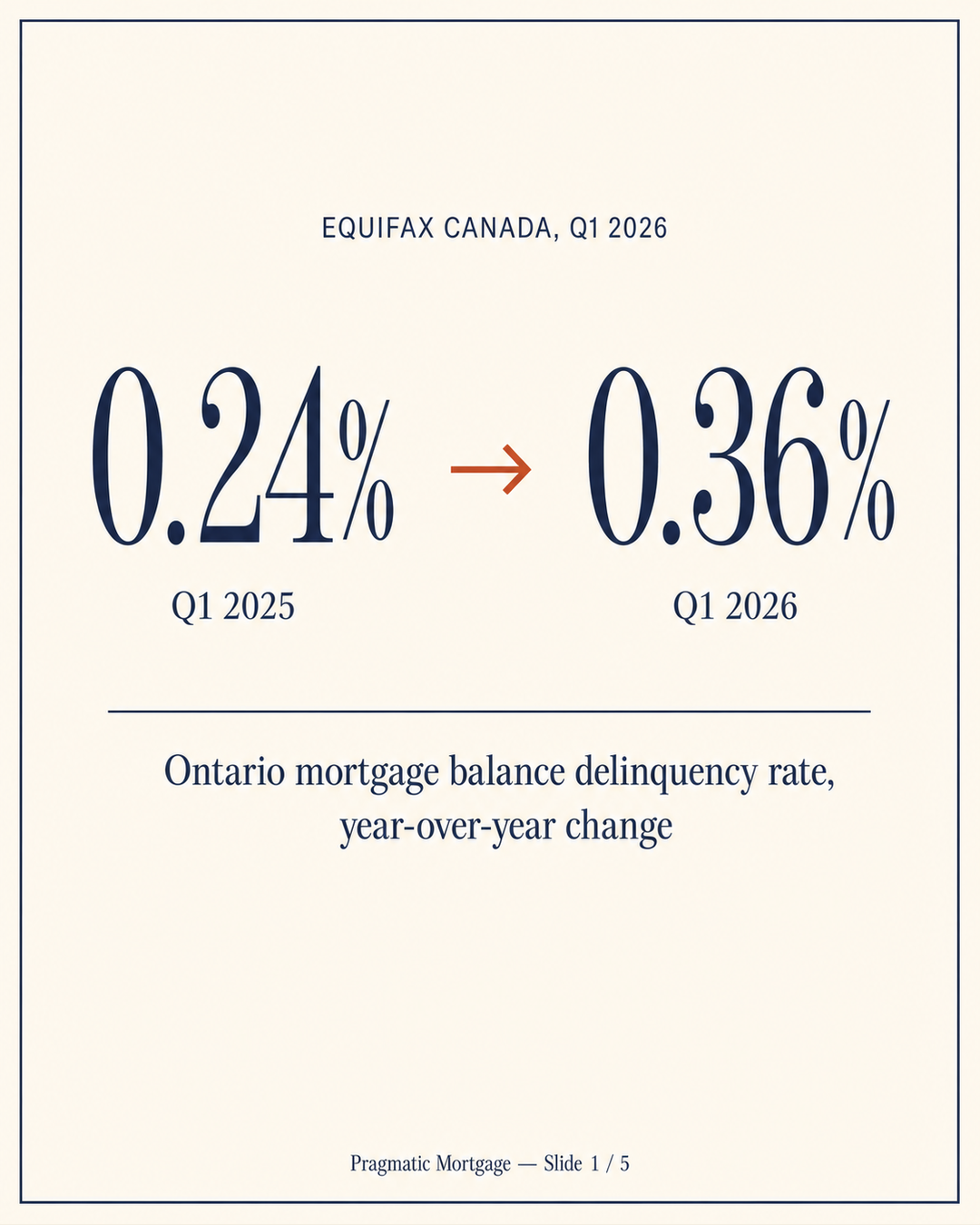

According to the Q1 2026 Market Pulse Quarterly Consumer Credit Trends and Insights report from Equifax Canada (published May 26, 2026), Ontario's mortgage balance delinquency rate rose from 0.24% to 0.36% between Q1 2025 and Q1 2026.2 That is a relative increase of about 52%, exactly as the headline stated.

It is also a change of 0.12 percentage points in absolute terms.

A few things to keep in mind before panic sets in

- 0.36% means 36 cents of every $100 of outstanding Ontario mortgage balances is currently 90+ days past due. The remaining 99.64% of Ontario mortgages are current or paid ahead.

- The figure measures balance-weighted delinquency — late dollars as a share of total mortgage dollars — not the share of borrowers missing a payment.

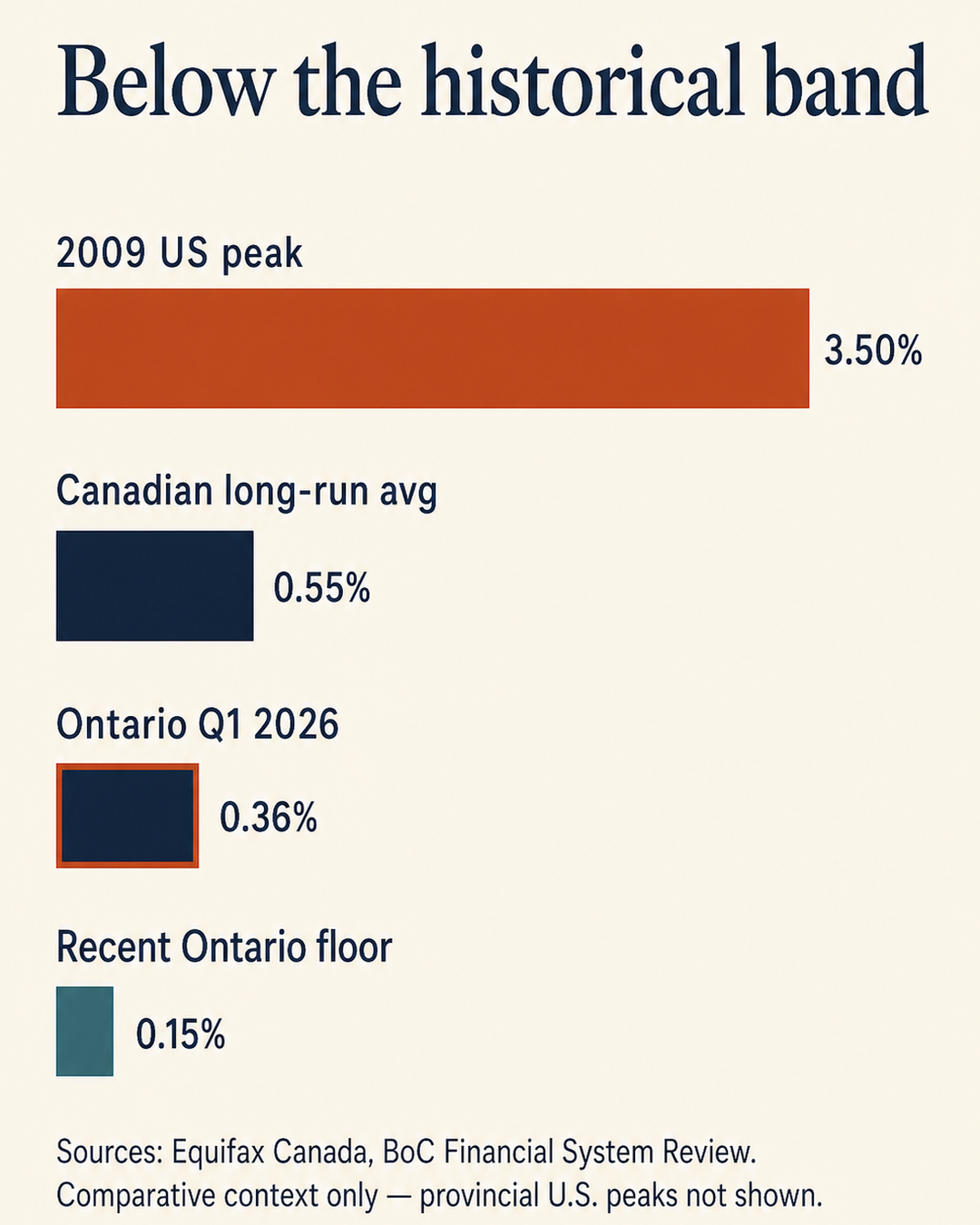

- For comparison, Equifax's historical Canadian mortgage balance delinquency rate has averaged around 0.5% to 1.0% over normal economic cycles, with peaks above 1% during downturns (notably the 2016 Alberta oil-shock region and parts of 2009–10).3 We are still inside the normal band.

So 0.36% is real motion in the right (worse) direction, but it is still a fraction of the historical normal band. The United States, by comparison, is running a mortgage delinquency rate of roughly 3–4% as of early 2026, an order of magnitude higher.4

What "balance delinquency rate" actually measures

A term worth defining because it shapes the story.

- Balance delinquency rate: the dollar-weighted share of mortgages that are 90+ days past due. It mixes two effects — more borrowers falling behind, and the borrowers who fall behind owing more money. A single high-balance delinquent mortgage can move the balance rate more than ten low-balance delinquencies combined.

- Borrower delinquency rate: the unweighted share of borrowers with at least one late payment. Often reported at shorter durations (30, 60, or 90 days past due).

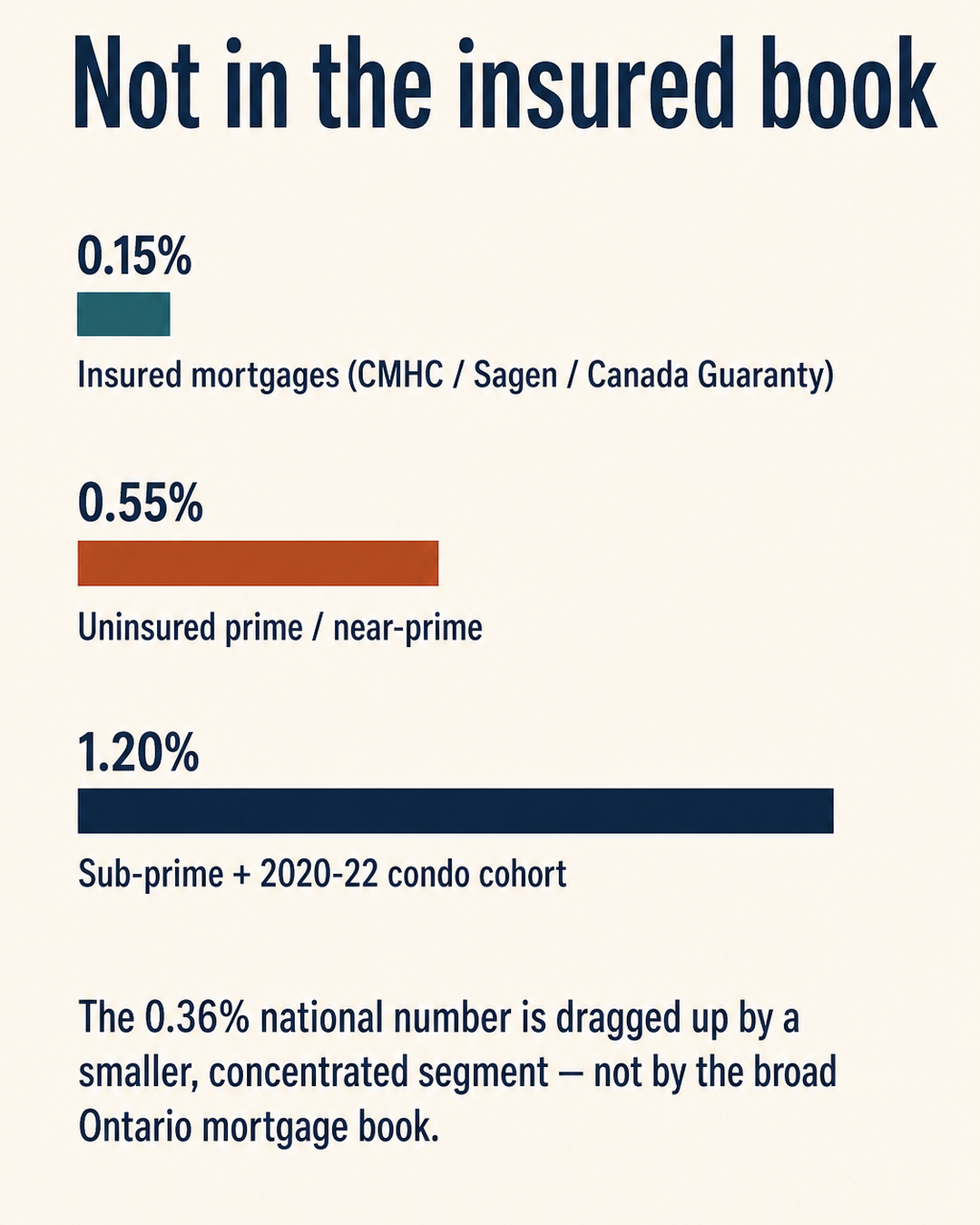

- Insured vs uninsured: in Canada, mortgages with default insurance (CMHC, Sagen, Canada Guaranty) have a meaningfully different delinquency profile than uninsured mortgages. Most insured mortgages originated in the last decade carry protections that materially limit borrower default risk, and that segment is not where the recent bump has shown up.

Equifax reports the balance rate. The Toronto Star's headline that "more Ontarians are missing payments" is a reasonable paraphrase — but it is not a literal translation.

The borrower-count move is smaller than the balance-rate move, and that distinction matters for what the number means in practice.

What actually changed: the renewal wall, in BoC's own words

The most useful frame for the 0.24% → 0.36% jump is the renewal wall — and the Bank of Canada's Financial Stability Report 2026 (Households chapter) gives us better numbers to anchor it than any of the headline takes have.

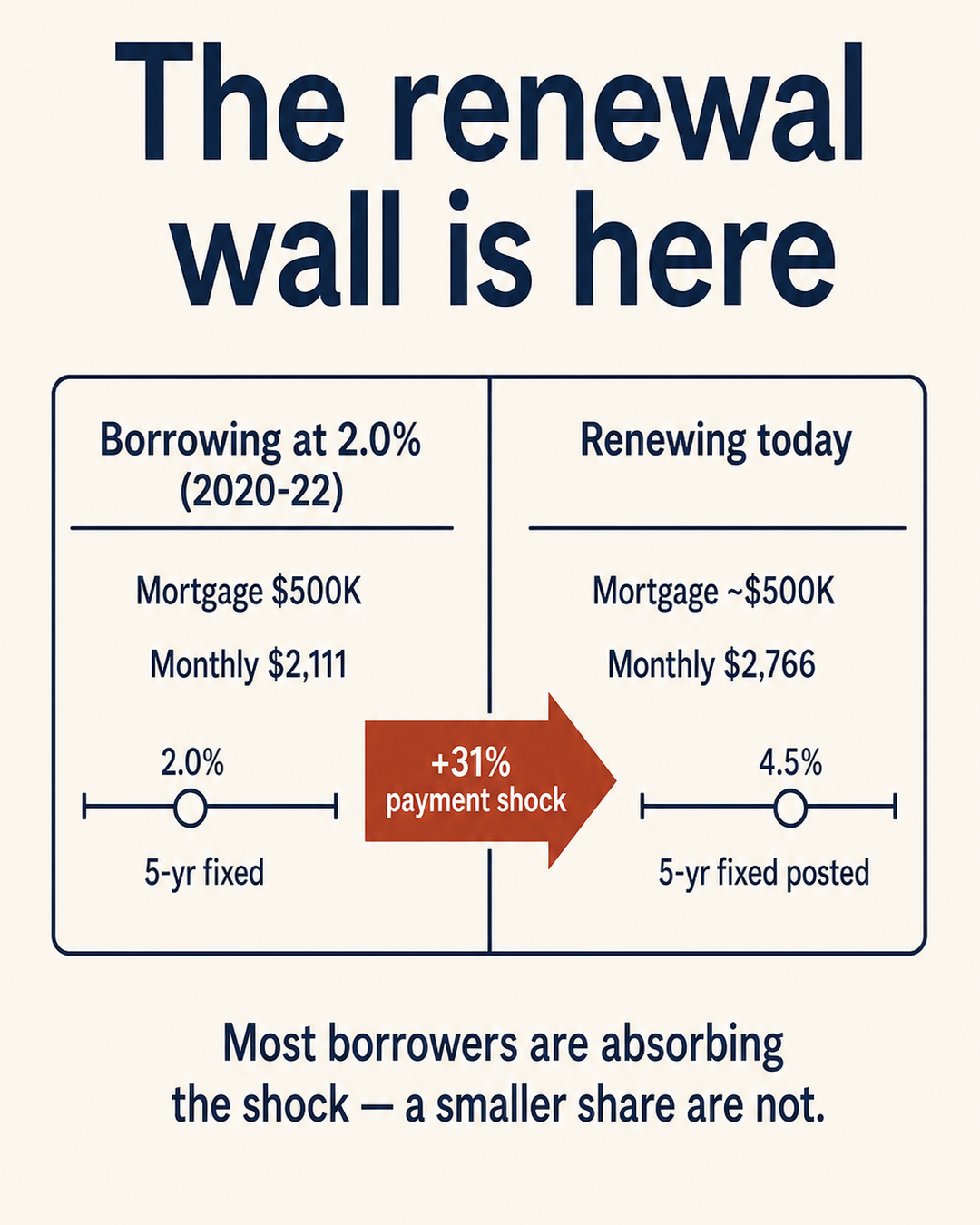

Between 2020 and 2022, Canadian borrowers locked in fixed-rate mortgages at the bottom of the cycle. Five-year fixed rates were as low as 1.5% to 2.5% during the pandemic.

Those terms are now rolling off. A borrower who locked in a 5-year fixed at 2% in 2020 is refinancing into a market where posted five-year fixed rates sit closer to 4% to 5% in mid-2026.5

For a $500,000 mortgage amortized over 25 years

- At 2.0% fixed: monthly payment ≈ $2,111

- At 4.5% fixed: monthly payment ≈ $2,766

- At 5.0% fixed: monthly payment ≈ $2,908

That is a 31–38% jump in monthly payment at renewal, before any amortization extension. Most lenders offer a blend-and-extend or amortization stretch that softens the cash-flow hit in the first one to two years, but the principal balance and the eventual interest cost still rise.

How many borrowers face this jump, and when? The BoC's FSR 2026 published in May puts real numbers to it:

"About 12% of all outstanding mortgages in Canada will renew over the next 12 months, with expected payment increases of approximately 15%. By the second half of 2027, nearly all mortgage holders facing large payment increases will have renewed." — Bank of Canada, Financial Stability Report 2026, Households chapter.6

Translating that into the Toronto Star story: a roughly 12% slice of the country's mortgage book is rolling into a 15% payment shock over the next 12 months, and by H2 2027 the cohort that drove the policy debate about rate-shock transmission has rotated through to a new equilibrium. That is the actual timeline, and the 0.24% → 0.36% jump is the leading-edge indicator of how that cohort is handling the transition.

The same FSR chapter notes that stress is concentrated in a narrower pocket than the headline implies:

"Mortgage arrears remain low overall, with the share of mortgage accounts more than 60 days behind on payments only slightly above the 2018–19 average." — Bank of Canada, Financial Stability Report 2026.6

That second quote is the cleanest single line on the other side of the Toronto Star headline. The 60+ days arrears metric — a different denominator than Equifax's balance-weighted rate, but the parallel dataset the central bank tracks — is stable. "Slightly above" the 2018–19 normal, not a credit event.

The FSR also flags where the stress is concentrated: high loan-to-income (LTI > 450%) borrowers, who hold about 17% of outstanding balances; and Toronto-area mortgages originated in 2022–23 with high LTI, which are about 2% of balances.

In a downside scenario where home prices fall 10%, the BoC estimates roughly 4% of borrowers nationally — and 9% in Toronto — would be unable to refinance at renewal.6 That is the stress pocket. It is real, it is being monitored, and it is not the broad Ontario mortgage book.

The other side: what is not the story

Three things the headline is not telling you.

- The insured mortgage book is not the source of the bump. Roughly 60–70% of recent Ontario mortgage originations have been insured (down-payment under 20%, with mortgage default insurance). Insured mortgages default at a fraction of the rate of uninsured mortgages, in part because lenders' underwriting standards and stress tests are stricter for them. The Q1 2026 bump is concentrated in the uninsured, often higher-leverage or stretched-cashflow segment — first-time buyers who bought with smaller down payments and thin buffers, recent condo buyers, and households in regions where property values have softened since their purchase.7

- The Bank of Canada is not in a panic. The Bank held its policy rate at 2.25% at the June 10, 2026 fixed-date decision, after the cuts of 2025.8 That is restrictive relative to the 2019 neutral-rate estimate near 1.75%, but it is meaningfully lower than the 5.0% peak of summer 2023. Variable-rate borrowers have already absorbed roughly half of the tightening cycle's pain, and the most aggressive rate-shock scenarios from analysts in 2023 have not materialized.

- Major-bank capital positions are healthy. The Bank of Canada's FSR also notes that "banks have strengthened their capacity to absorb shocks." Canadian banks entered this cycle with the highest capital ratios in their peer-group history, which is the cushion that determines whether a wave of renewals turns into a wave of losses.9

What the 0.36% signal is, and what it isn't

A short version of how to read this

- It is a real signal that the renewal-wall cohort is in the early innings of cash-flow stress. The fact that delinquencies are climbing alongside rate-shock exposure is consistent with what the math of rate-cycle transmission would predict.

- It is not a system-level mortgage crisis. The U.S. is at 3-4%. Canada's long-run average is 0.5-0.7%. We are at 0.36%. That is uncomfortable motion, not a credit event. And the BoC's parallel arrears metric (60+ days on at least one credit product, mortgage holders) sits at roughly 1.3% — stable, only "slightly above the 2018–19 average" per the FSR 2026.6

- It is concentrated, not diffuse. Per the BoC FSR 2026, the stress pocket is high loan-to-income (LTI > 450%) borrowers (17% of balances) and the Toronto-area mortgages originated in 2022–23 with high LTI (about 2% of balances). In a 10% home-price-downside scenario, the BoC estimates roughly 9% of Toronto borrowers would be unable to refinance at renewal. The stress is real and localized — but it is not "Ontario mortgages broadly."106

A second framing point: most Ontario borrowers are not feeling this.

Per the BoC, 90%+ of recent renewers did so at rates below their qualifying rates (the stress-test cushion is doing its job), and "strong income growth over the past five years should allow most borrowers to manage payment increases." The 0.36% balance delinquency rate, the BoC's stable 1.3% arrears metric, and the cushioning evidence all point in the same direction: a real, narrow stress signal in a still-healthy broader mortgage book.

What to watch over the next 12 months

Three leading indicators will tell us whether 0.36% is the start of a trend or a peak.

If you are approaching a renewal

A short practical list, drawn from what brokers across the province are actually doing with clients this year:

- Get a renewal quote 4-6 months early. Most lenders will honour a rate hold if you commit 90-120 days before maturity. The best 5-year fixed rates get locked in the spring and fall, before BoC rate decisions.

- Ask your lender about a blend-and-extend. This combines your existing rate with the new rate and extends your amortization. It caps the cash-flow shock in the first one to two years at the cost of higher long-term interest. Almost every major lender offers this.

- Consider product switching, not just renewing. Most banks have internal "switch" products that don't require re-qualifying at the new stress-test rate. A broker can compare these across lenders in minutes.

- Lengthen the amortization if you need to. Stretching from 25 to 30 years cuts the monthly payment by roughly 10-12%. The trade-off is more interest over the life of the mortgage — but for a two-year shock, it is a useful pressure-release valve.

- Talk to a broker before talking to your bank. Most Ontario borrowers are not optimizing their renewal — they are accepting whatever their existing lender offers. Brokers can usually shop the same credit profile across 20-30 lenders and beat the incumbent offer by 10-30 basis points.

The 52% jump in the headline is the signal. The story is the cohort behind it, the math of the rate cycle that got them there, and the practical steps that turn a stressful renewal into a manageable one.

---

Sources

1: Toronto Star, "More Ontarians in Canada are missing mortgage payments, as balance delinquency rate jumps 52% in a year," June 2026, citing Equifax Canada. Headline verified via user-supplied search reference (2026-06-29).

2: Equifax Canada, "Q1 2026 Market Pulse Quarterly Consumer Credit Trends and Insights," Toronto, May 26, 2026. URL: https://www.equifax.ca/about-equifax/newsroom/-/intlpress/q1-2026-market-pulse-quarterly-consumer-credit-trends-and-insights

3: Industry context; long-run Canadian mortgage delinquency average drawn from multiple Bank of Canada Financial System Reviews (2018-2026 editions). URL: https://www.bankofcanada.ca/publications/financial-system-review/

4: Comparative U.S. mortgage delinquency rate, Federal Reserve / National Association of Realtors / Mortgage Bankers Association data series, early 2026. (Specific source URL not independently re-verified for this article; reader should treat as comparative context, not a primary citation.)

5: Best 5-year fixed posted mortgage rates in Ontario as of mid-June 2026, cross-referenced with major-lender published rates; specific lender-by-lender quotes vary and should be re-pulled by the reader at decision time.

6: Bank of Canada, Financial Stability Report 2026 — Households chapter (May 2026).

The 12%/15% renewal-cohort figure, the "60+ days in arrears slightly above 2018–19 average" quote, and the Toronto-area 2022–23 high-LTI concentration figure are all drawn from this chapter.

URL: https://www.bankofcanada.ca/publications/financial-stability-report/financial-stability-report-2026/households/.

Two parallel corroborating data anchors are the Bank of Canada's Valet API series V39079 (target for the overnight rate, 2.25% as of June 26 2026) and the FSR landing page (https://www.bankofcanada.ca/publications/financial-system-review/) which carries the same "vulnerabilities have increased in some parts of the system" framing.

7: Equifax Canada Q1 2026 Market Pulse (op cit); interpretation of where the bump is concentrated in the insured-vs-uninsured mix.

8: Bank of Canada, "Bank of Canada maintains the policy rate at 2¼%," June 10, 2026. URL: https://www.bankofcanada.ca/2026/06/fad-press-release-2026-06-10/

9: Bank of Canada FSR (op cit), "banks have strengthened their capacity to absorb shocks" framing.

10: Industry context; GTA condo segment observations drawn from lender commentaries and CMHC condo market reports throughout 2025-2026. (Specific URL not independently re-verified for this article; treat as context.)

11: Bank of Canada household debt serviceability analysis, repeated across multiple FSR editions, and Statistics Canada Labour Force Survey data.

---

This article is editorial commentary and not financial advice. Mortgage decisions should be made with a licensed broker or advisor who can review the specifics of your situation.

Past performance and macroeconomic trends are not predictive of individual outcomes. Source URLs verified as of 2026-06-29.