TL;DR

Use this news update to understand how rate movements change qualification, renewal strategy, and payment risk before locking in a mortgage decision. The practical path is to compare qualification certainty, total borrowing cost, and execution reliability at the same time.

Why this matters now

Canadian borrowers are still dealing with rate volatility, and monthly payment risk can move faster than most household budgets.

Bank of Canada policy communication and lender repricing can diverge in timing, which is why borrowers need a process, not just a one-time quote.

The practical advantage comes from pre-planning your trigger points for fixed, variable, refinance, and renewal decisions before rates move again.

Pragmatic decision framework

- Start with payment resilience: model current payment, stress case payment, and renewal payment.

- Separate headline rate from total borrowing cost, including penalty risk and break flexibility.

- Review how contract structure (fixed, variable, open, closed) changes your downside in a volatile cycle.

- Re-check pre-approval and qualification assumptions whenever your timeline or debt profile changes.

Key signals from the research and prior article version

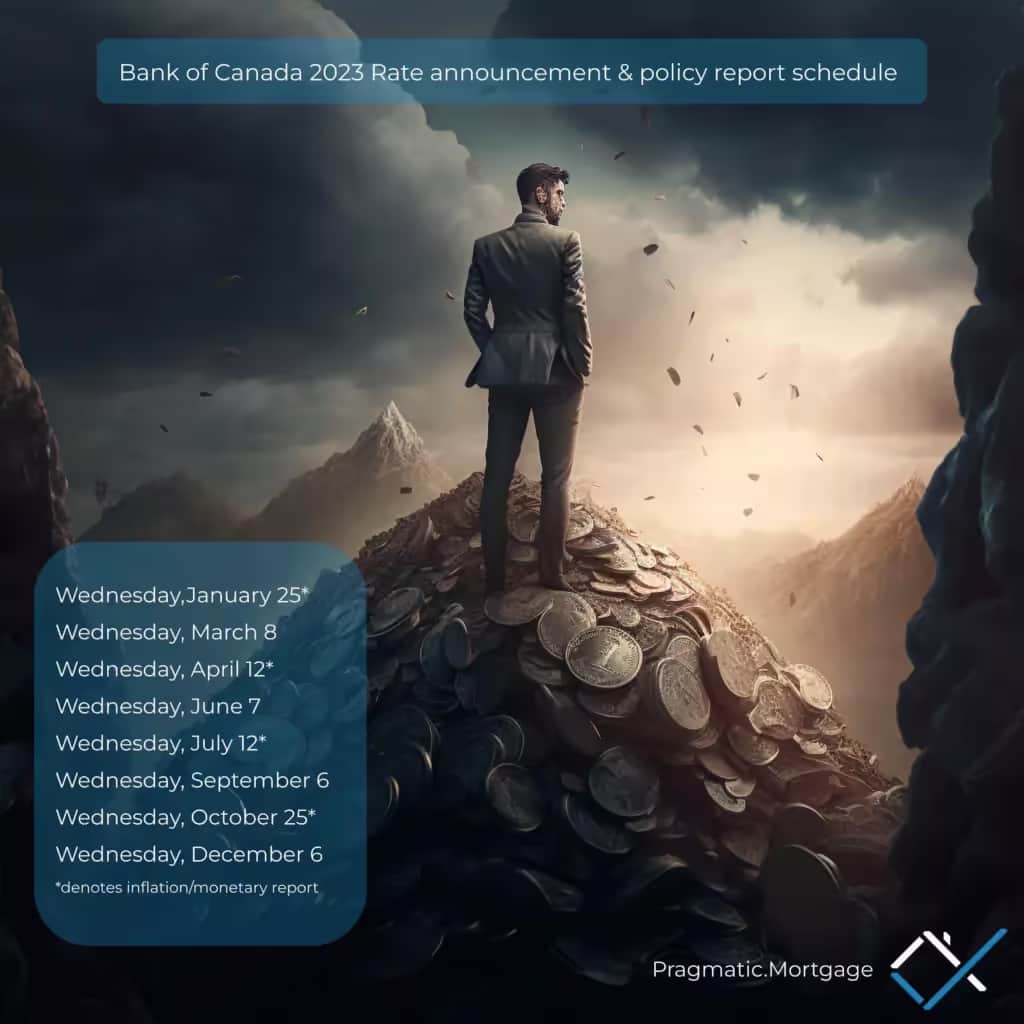

- Interest rate announcements in 2023 The Bank of Canada has recently announced its schedule for interest rate announcements in 2023.

- The Bank of Canada has been holding its interest rate at a record low of 0.25% since March 2020 due to the economic fallout from the COVID-19 pandemic, but it will likely start increas…

- 2023 Outlook Overall, the schedule of interest rate announcements by the Bank of Canada will be closely watched throughout 2023 as the economy continues to recover from the pandemic.

- The central bank will be making its interest rate announcements on the following dates: January 19, March 9, April 13, May 25, July 13, September 7, October 19, and December 7.

- The interest rate, also known as the overnight rate, is the rate at which banks can borrow money from the Bank of Canada overnight.

- Start with payment resilience: model current payment, stress case payment, and renewal payment.

- Separate headline rate from total borrowing cost, including penalty risk and break flexibility.

- Review how contract structure (fixed, variable, open, closed) changes your downside in a volatile cycle.

- Re-check pre-approval and qualification assumptions whenever your timeline or debt profile changes.

Detailed analysis and borrower impact

Signal 1: Interest rate announcements in 2023 The Bank of Canada has recently announced its schedule for interest rate announcements in 2023. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 2: The Bank of Canada has been holding its interest rate at a record low of 0.25% since March 2020 due to the economic fallout from the COVID-19 pandemic, but it will likely start increasing rates in 2023 as the economy recovers. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 3: 2023 Outlook Overall, the schedule of interest rate announcements by the Bank of Canada will be closely watched throughout 2023 as the economy continues to recover from the pandemic. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 4: The central bank will be making its interest rate announcements on the following dates: January 19, March 9, April 13, May 25, July 13, September 7, October 19, and December 7. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 5: The interest rate, also known as the overnight rate, is the rate at which banks can borrow money from the Bank of Canada overnight. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 6: Why is this important In general, when the Bank of Canada raises interest rates, it is trying to slow down the economy and curb inflation. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Cost, risk, and downside controls

Mortgage outcomes improve when you model downside early. Do not rely on a best-case rate or timeline assumption.

Before signing, pressure-test payment resilience, penalty exposure, and close-certainty risk under non-ideal conditions.

- Assuming policy announcements instantly flow through to every lender product.

- Chasing the lowest teaser rate without reviewing penalty terms and break scenarios.

- Locking strategy too early without a timeline-based fallback path.

- Ignoring the spread between posted and discounted rates when estimating penalties.

Behavioral traps that cause expensive mortgage decisions

These are the most common decision errors we see in live files, and the practical counter-move for each.

| Mental model | Typical trap | Pragmatic correction |

|---|---|---|

| Anchoring | Borrowers anchor to yesterday’s rate and miss total-cost trade-offs. | Anchor to worst-case monthly payment and 3-year total cost instead. |

| Present Bias | The immediate payment can feel more important than future refinance flexibility. | Score options on both month-one affordability and break-cost risk. |

| Status-Quo Bias | Staying with the current lender by default can hide better fit options. | Run a structured renewal comparison 90–120 days before maturity. |

Implementation plan: 7, 30, and 90 days

- Within 7 days: map your current mortgage, renewal date, and penalty formula.

- Within 30 days: run side-by-side scenarios for fixed, variable, and transfer options.

- Within 90 days: align your selected strategy with documentation readiness and lender timelines.

- Before commitment: confirm final pricing, payment sensitivity, and break-cost math in writing.

Scenario planning prompts

Scenario 1: If rates rise another 1%, can your budget absorb the payment without adding revolving debt? Build a response path before this scenario happens.

Scenario 2: If rates fall, does your contract allow a low-friction switch or refinance that still makes economic sense? Build a response path before this scenario happens.

Scenario 3: If your income changes, does your chosen term still preserve renewal or transfer flexibility? Build a response path before this scenario happens.

Questions to ask before you commit

Publication details

Published 2023-01-17. Last updated 2026-02-21.

This page was rewritten as part of the canonical CMS content rebuild, with a practical borrower-first structure and updated source references.

Best next step

Use this update to set a rate-response playbook before your next commitment window.

If your file has multiple constraints (income variability, debt pressure, short timelines, or penalty complexity), convert this page into a documented action plan before selecting a lender.

FAQ

Should I choose fixed or variable right now?

Choose based on payment resilience and timeline, not prediction. If uncertainty tolerance is low, fixed may suit better; if flexibility matters and you can absorb volatility, variable can still be viable.

How often should I review rate strategy?

Review at major lifecycle events and at least quarterly during volatile periods, then perform a full comparison 90 to 120 days before renewal.

What is the most important takeaway from The Bank of Canada has announced its schedule for interest rate announcements in 2023.?

Interest rate announcements in 2023 The Bank of Canada has recently announced its schedule for interest rate announcements in 2023. The central bank will be making its interest rate announcements on the following dates: January 19, March 9, April 13, May 25, July 13, September 7, October 19, and December 7. Focus on q…

How does this affect qualification and approval risk?

Use the decision framework in this page to stress-test debt-service, documentation quality, and lender policy fit before submitting a final commitment.

What should I verify with a lender or broker before acting?

Verify penalty structure, document requirements, closing timeline, and any assumptions that materially change payment or approval certainty.

What is a common mistake borrowers make on this topic?

Assuming policy announcements instantly flow through to every lender product.

How do I convert this guidance into action this month?

Within 7 days: map your current mortgage, renewal date, and penalty formula. Within 30 days: run side-by-side scenarios for fixed, variable, and transfer options.

What evidence should I keep in mind from this article?

Interest rate announcements in 2023 The Bank of Canada has recently announced its schedule for interest rate announcements in 2023.