What an assumable mortgage is — and what it is not

An assumable mortgage is a mortgage contract that allows a qualified buyer to step into the seller's existing mortgage — taking over the remaining balance, interest rate, remaining term, and original contract terms — instead of discharging the old mortgage and originating a new one. The buyer becomes the borrower on the existing mortgage; the seller's obligation transfers (ideally) to the buyer.

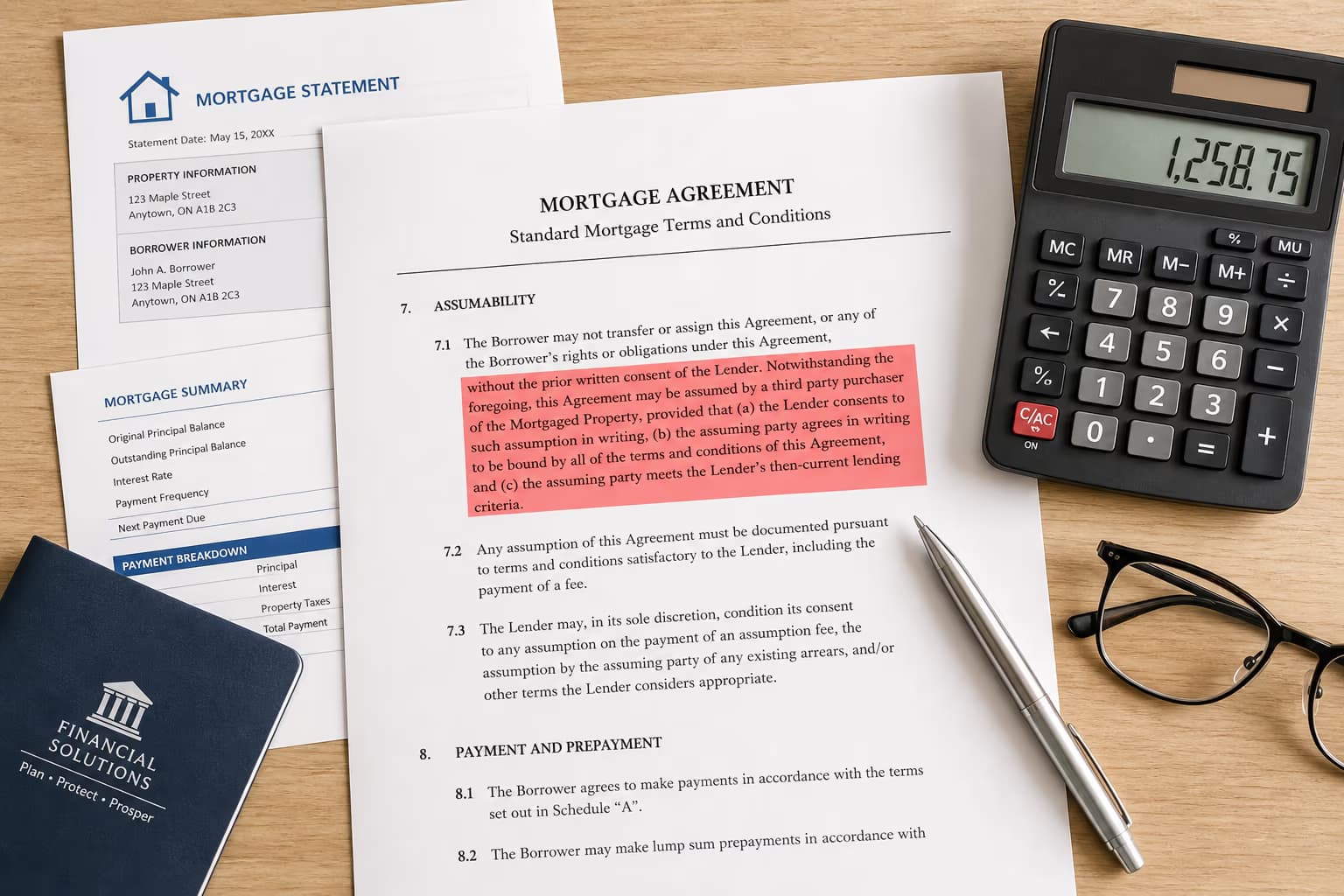

Assumability is not a legal right in Canada — it is a contractual feature written into the mortgage agreement. It requires the lender's explicit approval, and the lender can refuse the assumption for any reason. The buyer must go through the same qualification process as any new mortgage applicant, and the seller must be formally released from liability.

The core value proposition is simple: if the seller locked in a fixed rate at 2.89% in 2021 and current 5-year fixed rates are 4.79%, the buyer can potentially save hundreds of dollars per month by assuming the below-market rate rather than originating a new mortgage at current rates. But the rate advantage must survive every other cost, fee, and constraint in the transaction.

- Assumable means the mortgage contract allows assumption — it does not guarantee the lender will approve.

- The buyer still qualifies under current rules; the seller's original approval terms are irrelevant.

- Rate preservation is the main win, but only when the total transaction math supports it.

Which mortgages are assumable — and which are not

Assumability depends on the mortgage type, the lender, and whether default insurance is involved. Not all mortgage products allow assumption, and even when the contract technically permits it, the lender may impose conditions that make it impractical.

| Mortgage Type | Assumable? | Key Conditions |

|---|---|---|

| Conventional fixed-rate (major bank) | Usually yes | Buyer must qualify under current rules; lender approval required; seller release required. |

| Conventional variable-rate (major bank) | Rarely | Most variable-rate contracts do not include an assumability clause. Check the contract. |

| Insured fixed-rate (CMHC/Sagen/CG) | Sometimes | Insurer must consent; premium may apply; fewer lenders offer insured assumption. |

| Insured variable-rate | Almost never | Insurer and lender both typically require a new mortgage origination. |

| Alternative / private lender | Rarely | Most alternative mortgages are non-assumable by design; check contract language. |

| HELOC or collateral charge | No | Collateral charge mortgages and HELOCs are tied to the original borrower and are generally non-assumable. |

| Credit union (fixed) | Varies | Provincial credit union rules differ; some Manitoba and BC credit unions permit assumption. |

| Monoline lender (fixed) | Sometimes | MCAP, First National, and other monoline lenders may permit assumption on select products — verify with the lender. |

Always verify assumability directly with the lender before making an offer contingent on assumption. Lender policies change, and the specific mortgage contract governs.

The assumption process — step by step

Assuming a mortgage is not a simple name change. It is a full underwriting event with legal, financial, and administrative steps that can take 30–60 days. Understanding the sequence prevents delays and deal collapse.

- 1Confirm assumability

Review the seller's mortgage contract for the assumability clause. Contact the lender directly — do not rely on the seller's recollection or the real estate listing. The lender confirms in writing whether assumption is permitted and under what conditions.

- 2Buyer applies for qualification

The buyer submits a full mortgage application to the lender, including income verification, credit check, employment confirmation, and down payment/equity gap source documentation. This is identical to a new mortgage application.

- 3Lender underwrites the buyer

The lender assesses the buyer's income, credit, debt-service ratios (GDS/TDS), and stress test against the assumed mortgage's remaining balance and payment. The seller's original approval terms are irrelevant.

- 4Property appraisal may be required

The lender may order a new appraisal to confirm the property's current market value. If the appraisal comes in below the purchase price, the buyer must cover the difference in addition to the equity gap.

- 5Seller release negotiation

The seller and lender negotiate the release — the seller must be formally discharged from the mortgage obligation. Without a full release, the seller remains liable for the mortgage even after transferring the property.

- 6Equity gap funding confirmed

The buyer proves they have verified funds to cover the gap between the purchase price and the remaining mortgage balance. This is typically cash but may include approved secondary financing.

- 7Legal close

The buyer's lawyer registers the assumption, the transfer of title, and any secondary financing. The seller's lawyer confirms the release. Funds flow, keys transfer, and the buyer becomes the borrower on record.

Assumption is a sequence of seven distinct steps — treat it like a full mortgage application, not a shortcut.

The buyer must qualify under current rules — the seller's original approval means nothing to the lender.

Buyer qualification — the part that surprises most people

The single biggest misconception about assumable mortgages is that the buyer skips qualification. They do not. The lender treats the assumption as a new credit decision — the buyer must meet the lender's current underwriting standards, including income verification, credit score minimums, debt-service ratio limits, and the stress test where applicable.

For federally regulated lenders, the stress test applies: the buyer must qualify at the greater of the contract rate plus 2% or 5.25%. If the assumed mortgage has a 2.89% rate, the buyer qualifies at 5.25% — not at the below-market rate they are assuming. This can be the deal-breaker for buyers who are stretched on affordability.

The buyer also needs to show down payment or equity gap funds. If the purchase price is $700,000 and the assumed mortgage balance is $400,000, the buyer must bring $300,000 to closing — not as a down payment, but as the equity gap. Lenders verify the source of these funds with the same scrutiny applied to down payment verification.

- Buyer income must support the assumed payment under current GDS/TDS limits.

- Credit score minimums apply — typically 620–680 for conventional mortgages.

- Stress test applies at 5.25% or contract rate + 2%, whichever is higher.

- Equity gap funds must be verified — same documentation as a down payment.

Seller release — the liability trap most sellers miss

When a seller transfers a mortgage through assumption, the default position is that the seller remains liable on the mortgage unless the lender provides a formal, written release. This means that if the buyer defaults two years after closing, the lender can pursue the original seller for the outstanding balance.

A full release discharges the seller from all obligations under the mortgage contract. A partial release may limit the seller's liability but not eliminate it entirely. A “covenant not to sue” is weaker than a release — it means the lender promises not to pursue the seller, but the promise may not survive if the mortgage is sold or assigned to another institution.

Most major Canadian banks will provide a full release when the buyer qualifies independently and the assumption is formalized through legal channels. However, some lenders charge a release fee ($250–$500), and the process can add 2–4 weeks to the closing timeline. The seller should not accept an offer contingent on assumption without confirming that a full release is available and understanding the timeline.

- Insist on a full, written release — not a partial release or covenant not to sue.

- Confirm the release timeline with the lender before accepting an assumption-contingent offer.

- Budget for a release fee ($250–$500 at most major lenders).

- If the lender refuses to release, the assumption is not viable for the seller.

Seller release must be confirmed in writing — liability can survive the property transfer.

The equity gap is the single biggest deal-killer in assumption transactions.

The equity gap — the hidden math that kills most assumption deals

The equity gap is the difference between the purchase price and the remaining mortgage balance being assumed. It is the single biggest reason assumable mortgage deals collapse — buyers fall in love with the low rate but cannot cover the gap.

Equity Gap = Purchase Price − Remaining Mortgage Balance

Example: A seller lists their home for $700,000 with a remaining mortgage balance of $320,000 from a 2019 origination. The equity gap is $380,000. The buyer must bring $380,000 to closing in cash or approved secondary financing — on top of closing costs (1.5%–4%, or $10,500–$28,000).

Most buyers who are attracted to assumable mortgages are rate-sensitive — they want the lower payment. But rate-sensitive buyers are often the least equipped to cover a large equity gap. If the buyer only has a 5% down payment ($35,000 on $700,000), but the equity gap is $380,000, the numbers do not work without extensive secondary financing.

Secondary financing options — second mortgages, private loans, or family gifts — can bridge the gap, but they add complexity, cost, and risk. A second mortgage at 8%–12% on the gap amount may erase the savings from the assumed low rate. The buyer must compare the blended cost of assumption + gap financing against a single new mortgage at current rates.

Assumable mortgage vs new mortgage — what to compare

The decision to assume or originate a new mortgage is a math problem, not a rate comparison. The assumed rate can look attractive in isolation but lose when all costs, constraints, and risks are included.

| Factor | Assume Existing Mortgage | New Mortgage |

|---|---|---|

| Interest rate | Preserves below-market rate (e.g., 2.89%) | Current market rate (e.g., 4.79%) — higher monthly payment |

| Buyer qualification | Full underwriting required — income, credit, stress test | Full underwriting required — same standard process |

| Cash to close | Equity gap + closing costs — can be $300K+ | Down payment (5%–20%) + closing costs — typically lower |

| Remaining term | Limited to the seller's remaining amortization | Full 25–30 year amortization available |

| Prepayment privileges | Inherits seller's contract — may have limited prepayment options | Full current-market prepayment terms and portability |

| Rate hold period | None — rate is locked at contract rate | Typically 90–130 day rate hold available |

| Seller release | Requires formal lender release — timeline risk | Not applicable — seller is discharged at closing |

| Portability | Usually non-portable — tied to the specific property | Standard portability options available with new mortgage |

| Secondary financing | Often required to cover equity gap — adds cost and complexity | Rarely needed — standard down payment structure |

| Legal costs | Higher — assumption registration + standard closing costs | Standard — discharge of old mortgage + new registration |

The rate is only one variable — compare the full financial picture, not just the monthly payment.

When assuming makes sense — and when it does not

Assumable mortgages are not universally good or bad — they are situational. The spread between the assumed rate and current market rates, the buyer's cash position, the seller's equity, and the remaining term all determine whether assumption is the right path.

- ✓The seller's rate is at least 1.5 percentage points below current market rates.

- ✓The buyer has enough verified cash to cover the equity gap without expensive secondary financing.

- ✓The remaining term is 3+ years — enough time for the rate savings to compound.

- ✓The lender provides a full seller release with a confirmed timeline.

- ✓The buyer qualifies comfortably at the stress test rate with the assumed payment.

- ✓The mortgage contract has standard prepayment privileges and reasonable terms.

- ✗The rate spread is less than 1 percentage point — savings are marginal.

- ✗The equity gap is so large the buyer needs a high-interest second mortgage to bridge it.

- ✗The remaining term is under 2 years — the rate advantage expires before it pays back.

- ✗The lender cannot confirm a full seller release within the closing timeline.

- ✗The buyer barely qualifies at the stress test — one change in circumstances breaks the deal.

- ✗The mortgage has restrictive prepayment terms, no portability, or high discharge penalties.

Major Canadian lender policies on assumable mortgages

Each major Canadian lender has its own assumability policy. Policies change over time, so always verify directly with the lender. The table below summarizes the general policy positions as of May 2026 for conventional fixed-rate mortgages.

| Lender | Assumability Policy | Qualification Required | Seller Release | Fee |

|---|---|---|---|---|

| RBC Royal Bank | Permitted on most conventional fixed-rate mortgages | Yes — full underwriting | Full release available | $300–$500 |

| TD Canada Trust | Permitted on conventional fixed-rate products | Yes — full underwriting | Full release available | $250–$400 |

| Scotiabank | Permitted on select fixed-rate mortgages | Yes — full underwriting | Full release available | $300–$500 |

| BMO Bank of Montreal | Permitted on most conventional fixed-rate mortgages | Yes — full underwriting | Full release available | $300 |

| CIBC | Permitted on conventional fixed-rate mortgages | Yes — full underwriting | Full release available | Varies |

| National Bank | Permitted on select products | Yes — full underwriting | Full release available | $300–$500 |

| Desjardins | Permitted on conventional fixed-rate caisse loans | Yes — full underwriting | Full release available; provincial rules apply | Varies by caisse |

| MCAP | Product-dependent; contact lender | Yes — full underwriting | Case-by-case | Contact lender |

| First National | Product-dependent; contact lender | Yes — full underwriting | Case-by-case | Contact lender |

| Meridian Credit Union | Permitted on select fixed-rate mortgages (Ontario) | Yes — full underwriting | Full release available | $300–$450 |

Policies as of May 2026. Always confirm directly with the lender — policies can change without notice. Insured mortgages (CMHC/Sagen/CG) and variable-rate products have different rules. Contact a licensed mortgage broker for current lender-specific guidance.

Legal and administrative costs add up — budget for them before committing to assumption.

Professional costs, legal requirements, and tax considerations

An assumption transaction incurs professional costs on both sides that are distinct from a standard purchase transaction. The buyer and seller should budget for these costs separately — they cannot be rolled into the assumed mortgage balance.

- Legal fees for assumption: $1,000–$1,800 — higher than a standard purchase because the lawyer must register the assumption with the land title office and coordinate the seller release.

- Lender assumption fee: $250–$500 — charged by the lender to process the assumption application and underwriting review.

- Seller release fee: $250–$500 — charged by the lender to formally discharge the seller from liability.

- Appraisal fee: $350–$600 — if the lender requires a new appraisal (common for assumption transactions).

- Title insurance: $250–$500 — the buyer typically needs a new title insurance policy; the seller's policy does not transfer.

- Provincial land transfer tax: Varies by province — the buyer pays LTT on the purchase price, same as any property purchase. Alberta and Saskatchewan buyers pay only nominal registration fees.

- GST/HST: Does not apply to resale residential properties. Applies to new construction only.

- Property tax adjustments: Prorated between buyer and seller based on possession date — standard for all transactions.

Frequently asked questions

Are all mortgages in Canada assumable?

No. Assumability is a contractual feature, not a legal right. Conventional fixed-rate mortgages with major Canadian banks are the most commonly assumable. Variable-rate mortgages, insured mortgages (CMHC/Sagen/CG), HELOCs, collateral charge mortgages, and most alternative-lender mortgages are generally not assumable. Always verify the specific mortgage contract and confirm with the lender.

Does the buyer still have to qualify for an assumable mortgage?

Yes — and this is the most common misconception. The buyer must qualify under the lender's current underwriting rules, including income verification, credit score minimums, debt-service ratio limits (GDS/TDS), and the stress test where applicable. The seller's original approval terms are irrelevant. For federally regulated lenders, the buyer qualifies at the greater of the contract rate + 2% or 5.25%.

What is the equity gap and how is it calculated?

The equity gap is the difference between the purchase price and the remaining mortgage balance being assumed. Formula: Equity Gap = Purchase Price − Remaining Mortgage Balance. For example, a $700,000 purchase price with a $320,000 remaining mortgage creates a $380,000 equity gap. The buyer must cover this gap with verified cash, approved secondary financing, or a combination. The equity gap is the most common reason assumable mortgage deals collapse — rate-sensitive buyers are often unable to cover a large gap.

Does the seller remain liable after the mortgage is assumed?

That depends on whether the lender provides a full written release. Without a full release, the seller remains liable on the mortgage even after transferring the property — meaning the lender can pursue the seller if the buyer defaults. A partial release or covenant not to sue provides weaker protection. The seller should insist on a full release confirmed in writing before accepting an assumption-contingent offer. Most major Canadian banks will provide a full release when the buyer qualifies independently, typically for a fee of $250–$500.

Is assuming a mortgage better than getting a new mortgage?

It depends on the numbers. Assumption wins when: (1) the assumed rate is at least 1.5 percentage points below current market rates, (2) the buyer can cover the equity gap with verified cash (not expensive secondary debt), (3) the remaining term is 3+ years, and (4) the seller receives a full release. Assumption loses when the equity gap forces expensive secondary financing that erases the rate savings, or when the remaining term is so short the advantage expires before it pays back the added complexity and legal costs.

How long does a mortgage assumption take?

A mortgage assumption typically takes 30–60 days from application to close — comparable to or slightly longer than a new mortgage. The timeline depends on the lender's assumption processing volume, the seller release negotiation, any appraisal requirements, and the buyer's documentation readiness. The seller should not accept an assumption-contingent offer with a closing date shorter than 45 days without confirming the lender's timeline in writing.

Can I port my assumable mortgage to a new property?

Most assumable mortgages are tied to the specific property and are not portable. Portability is a separate mortgage feature that allows the borrower to transfer the mortgage to a new property when they sell. If the mortgage is assumable, the buyer assumes it on the existing property — it does not move. If you need portability, compare a new mortgage with full portability options against the assumed rate advantage.

What are the tax implications of assuming a mortgage?

For principal residence purchases, there are generally no direct tax implications for the buyer or seller — the mortgage assumption itself does not trigger a taxable event. The buyer pays provincial land transfer tax on the purchase price (same as any purchase), which varies by province. Alberta and Saskatchewan charge only nominal registration fees. GST/HST applies to new construction only, not resale homes. The seller's principal residence exemption covers any capital gain on the sale. For investment properties, different tax rules apply — consult a tax professional.

Do credit unions offer assumable mortgages?

Some provincial credit unions permit mortgage assumption on conventional fixed-rate products — notably in Manitoba, British Columbia, and select Ontario credit unions. Credit union policies are governed by provincial regulations and the credit union's own lending rules, so policies vary significantly. Meridian Credit Union (Ontario) and Vancity (BC) are examples of credit unions that may permit assumption on select products. Always verify with the specific credit union.

What happens if the lender refuses the assumption?

If the lender refuses the assumption — which they can do for any reason — the deal falls through unless the buyer qualifies for a new mortgage. This is why assumption-contingent offers should include a financing condition that allows the buyer to pursue a new mortgage if the assumption is denied. The condition should allow at least 30–45 days for the lender to process the assumption application and provide a decision in writing.

Review your assumption with a licensed Canadian broker

Assumable mortgages are rare, valuable, and complex. Our brokers compare the assumed mortgage against new origination, secondary financing, and alternative paths — so you know whether the assumption saves money or costs more in the long run.