TL;DR

Use this news update to reduce long-term borrowing cost while preserving flexibility and avoiding avoidable refinance or break penalties. The practical path is to compare qualification certainty, total borrowing cost, and execution reliability at the same time.

Why this matters now

Many borrowers are entering renewal windows with materially different rate conditions than when their current term started.

A refinance or transfer can improve outcomes, but only if penalty math, break clauses, and timeline costs are modeled correctly.

Execution quality matters: a strong switch file closes on schedule with no surprises in payout statement and legal timing.

Pragmatic decision framework

- Estimate break cost using lender formula and compare against projected savings over your hold period.

- Model three paths: stay, switch, and refinance with cash-out assumptions.

- Include legal fees, appraisal requirements, and administrative friction in net-benefit calculations.

- Select the path that improves resilience and net cost, not only the path with the lowest posted rate.

Key signals from the research and prior article version

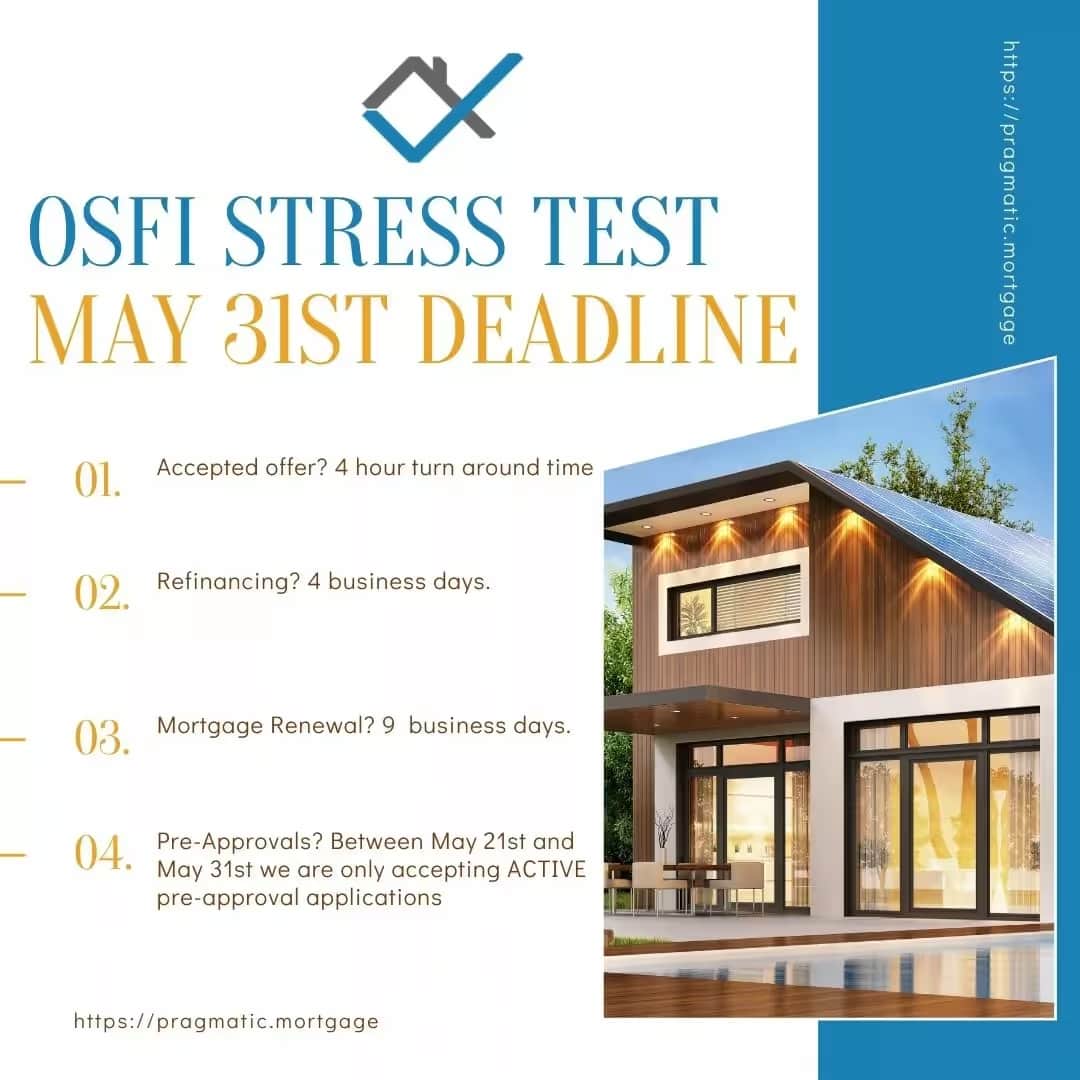

- OSFI has set the new stress test for uninsured (AND INSURED in the 11th hour, ouch) mortgages to take affect June 1st.

- The new stress test will affect your buying power by 5-10% in a purchasing power.

- We are going to try everything we possibly can to get you folks locked in to the OLD stress test for the next 120 days.

- Refinance applications Communication updates: 3-4 business days 3-6 weeks for final approval The banks are going to get SLAMMED with Refinance applications this week, and they are goin…

- Please note, we will not be accepting any further Refinance applications between May 27th and May 31st.

- Estimate break cost using lender formula and compare against projected savings over your hold period.

- Model three paths: stay, switch, and refinance with cash-out assumptions.

- Include legal fees, appraisal requirements, and administrative friction in net-benefit calculations.

- Select the path that improves resilience and net cost, not only the path with the lowest posted rate.

Detailed analysis and borrower impact

Signal 1: OSFI has set the new stress test for uninsured (AND INSURED in the 11th hour, ouch) mortgages to take affect June 1st. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 2: The new stress test will affect your buying power by 5-10% in a purchasing power. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 3: We are going to try everything we possibly can to get you folks locked in to the OLD stress test for the next 120 days. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 4: Refinance applications Communication updates: 3-4 business days 3-6 weeks for final approval The banks are going to get SLAMMED with Refinance applications this week, and they are going to throw them on the back burner to prioritize purchases first. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 5: Please note, we will not be accepting any further Refinance applications between May 27th and May 31st. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Signal 6: If you plan to tap into your current equity for future benefit, I can not stress this enough: There will be no better time to do this right now for the next 10 years. Practical implication: verify how this changes qualification reliability, payment resilience, or timeline certainty before committing.

Cost, risk, and downside controls

Mortgage outcomes improve when you model downside early. Do not rely on a best-case rate or timeline assumption.

Before signing, pressure-test payment resilience, penalty exposure, and close-certainty risk under non-ideal conditions.

- Comparing rates without netting out break penalties and closing costs.

- Ignoring collateral charge implications when planning future flexibility.

- Waiting too late in the renewal window and losing negotiating leverage.

- Assuming all lenders use the same penalty or prepayment formulas.

Behavioral traps that cause expensive mortgage decisions

These are the most common decision errors we see in live files, and the practical counter-move for each.

| Mental model | Typical trap | Pragmatic correction |

|---|---|---|

| Sunk Cost Fallacy | Borrowers stay in expensive terms because they already invested in the current mortgage. | Evaluate decisions on future cost and flexibility, not past commitment. |

| Regret Aversion | Fear of making the wrong move can lead to automatic renewal. | Use a documented compare-and-decide framework with explicit trigger points. |

| Default Effect | Auto-renew offers can become the default even when alternatives are stronger. | Schedule lender and broker comparisons before the renewal letter arrives. |

Implementation plan: 7, 30, and 90 days

- Within 7 days: collect payout statement, current term details, and penalty terms.

- Within 30 days: compare stay/switch/refinance outcomes using realistic hold periods.

- Within 90 days: lock final strategy and prepare all required documentation for smooth execution.

- Before commitment: confirm final penalty number and legal disbursement timing in writing.

Scenario planning prompts

Scenario 1: If you break now, when does savings overtake penalty and fees on a net basis? Build a response path before this scenario happens.

Scenario 2: If rates drop later, does your contract preserve enough flexibility to react? Build a response path before this scenario happens.

Scenario 3: If income tightens, which option protects monthly cash flow without excessive long-term cost? Build a response path before this scenario happens.

Questions to ask before you commit

Publication details

Published 2021-05-21. Last updated 2026-02-21.

This page was rewritten as part of the canonical CMS content rebuild, with a practical borrower-first structure and updated source references.

Best next step

Build a stay-versus-switch-versus-refinance scorecard before signing any renewal offer.

If your file has multiple constraints (income variability, debt pressure, short timelines, or penalty complexity), convert this page into a documented action plan before selecting a lender.

FAQ

When is refinancing worth it?

Refinancing is worth it when net savings or strategic benefits exceed penalties, fees, and risk adjustments over your expected hold period.

How early should I start renewal planning?

Start 120 days before maturity to preserve negotiation leverage and allow enough time for transfer or refinance underwriting.

What is the most important takeaway from OSFI Stress Test Deadline | May 31st?

OSFI has set the new stress test for uninsured (AND INSURED in the 11th hour, ouch) mortgages to take affect June 1st. The new stress test will affect your buying power by 5-10% in a purchasing power. Focus on qualification certainty, total cost, and timeline reliability before committing.

How does this affect qualification and approval risk?

Use the decision framework in this page to stress-test debt-service, documentation quality, and lender policy fit before submitting a final commitment.

What should I verify with a lender or broker before acting?

Verify penalty structure, document requirements, closing timeline, and any assumptions that materially change payment or approval certainty.

What is a common mistake borrowers make on this topic?

Comparing rates without netting out break penalties and closing costs.

How do I convert this guidance into action this month?

Within 7 days: collect payout statement, current term details, and penalty terms. Within 30 days: compare stay/switch/refinance outcomes using realistic hold periods.

What evidence should I keep in mind from this article?

OSFI has set the new stress test for uninsured (AND INSURED in the 11th hour, ouch) mortgages to take affect June 1st.

Sources

Common mistakes and preventive controls

- Making a decision off one quote without scenario comparisons.

- Skipping the document-readiness check until late in the process.

- Underestimating legal, appraisal, and timeline dependencies.

- Focusing on rate only and ignoring penalty architecture.

- Failing to define a fallback strategy before committing.